Mastering Workforce Strategy in 2025: The CFO’s Guide

The CFO’s Strategic Guide to Workforce Composition: A Data-Driven Analysis of Freelancers vs. FTEs

Introduction: Beyond the Budget Line Item—Workforce as a Strategic Asset

The decision to hire a full-time employee (FTE) versus engaging a freelancer is one of the most critical financial levers an agency can pull. Historically viewed through a narrow lens of immediate cost savings, this choice is, in fact, a foundational element of financial strategy. It dictates the very nature of an organization’s cost structure, shaping its resilience, scalability, and long-term profitability. The composition of a workforce is not merely a line item on a budget; it is a strategic asset that determines an agency’s capacity to navigate market volatility, absorb economic shocks, and capitalize on growth opportunities. If you want to understand more about how agencies should approach their overall financials and accounting infrastructure, see our Accounting for Marketing Agencies: A Primer for a foundational overview.

For the modern Chief Financial Officer, the dilemma is acute. On one hand, full-time employees offer stability, cultural integration, and deep institutional knowledge—invaluable assets for building a cohesive and reliable team. On the other hand, freelancers provide unparalleled flexibility, access to a global pool of specialized talent, and a variable cost model that aligns expenses directly with revenue generation. Navigating this tension requires moving beyond anecdotal evidence and gut-feel decisions. It demands a quantitative framework grounded in a granular understanding of true costs and their second-order effects on the financial health of the business.

This report provides that framework. It is designed to replace ambiguity with analysis, offering a data-driven methodology for making optimal workforce composition decisions. The analysis will proceed through five distinct stages:

- A deconstruction of the true, “fully loaded” cost of a full-time employee, moving far beyond base salary.

- A financial model of the “all-in” project cost of a freelancer, accounting for hidden management overhead.

- A direct analysis of how each labor model impacts project and agency-level profitability metrics.

- An examination of the strategic consequences for cash flow, risk management, and scalability.

- The presentation of a strategic decision matrix to guide optimal workforce planning for any given business need.

By the conclusion of this report, leaders will be equipped with a clear, defensible, and financially rigorous approach to building the most effective and profitable workforce for the future. For those leading agencies, understanding the role of accurate time tracking in service-based businesses is also essential, as labor is your most expensive and valuable resource.

I. The Anatomy of an Employee: Deconstructing the Fully Loaded Cost of an FTE

To make an informed comparison, it is imperative to first establish a precise financial baseline for the cost of a full-time employee. Gross salary represents only the visible tip of the iceberg; the true cost to the company (TCC), often referred to as the “fully loaded cost” or “labor burden,” includes a significant overlay of mandatory taxes, benefits, and overhead that can substantially increase the total expense. A widely used rule of thumb suggests that the TCC is typically 1.25 to 1.4 times the employee’s base salary. Data from the U.S. Bureau of Labor Statistics (BLS) corroborates this, indicating that in the private sector, benefits alone account for nearly 30% of an employee’s total compensation package. For accurate financial planning and a valid comparison against freelance alternatives, a detailed, line-item calculation is essential. If you find financial statements confusing or want to dive deeper, our detailed guide for agency owners can help clarify the numbers behind these cost models.

Step 1: Mandatory Employer-Paid Payroll Taxes (The Non-Negotiables)

These costs are legally mandated and represent the first layer of expense on top of gross wages. For an employer operating in California, these contributions are specific and substantial.

- Social Security: The employer is required to contribute 6.2% of an employee’s wages up to the annual Social Security wage base limit. For 2025, this cap is set at $176,100.

- Medicare: A contribution of 1.45% is required on all of an employee’s wages, with no upper limit or wage cap.

- Federal Unemployment Tax (FUTA): The standard FUTA tax rate is 6.0% on the first $7,000 of an employee’s annual wages. However, employers in states with compliant unemployment programs receive a credit of up to 5.4%, resulting in a net FUTA tax rate of 0.6%. This amounts to a maximum of $42 per employee per year.

- State Unemployment Insurance (SUI): This is a state-level tax, and in California, it is paid on the first $7,000 of an employee’s wages. The tax rate for new employers is 3.4% for the first two to three years of operation. For established employers, the rate can vary significantly, from 1.5% to 6.2%, depending on their employment history. For modeling purposes, the new employer rate of 3.4% provides a conservative baseline.

- Employment Training Tax (ETT): California employers are also subject to the ETT, which is 0.1% on the first $7,000 of wages, contributing to a state fund for worker training programs.

- Workers’ Compensation Insurance: This insurance provides benefits to employees who get injured or become ill from a work-related cause. Rates are highly dependent on the industry and the specific job classification’s risk profile. For low-risk professional roles, such as a marketing manager or software developer, a rate of approximately 1.2% of the gross salary is a reasonable estimate.

Step 2: The High Cost of Benefits (The Strategic Levers)

The benefits package is often the largest and most variable component of an employee’s TCC. While these costs are significant, they are also strategic investments in attracting and retaining top talent. The decision to offer a competitive benefits package is the primary factor that elevates an employee’s true cost from the lower end of the 1.25x multiplier toward the 1.4x range and beyond. While mandatory taxes add a predictable 8-10% to a salary, the benefits package can easily add another 15-30%. For a CFO, this means that the design of the benefits program is a primary lever for managing the overall labor burden.

- Health Insurance: This is a cornerstone of any competitive benefits package and a major financial commitment for the employer. According to the 2025 Employer Health Benefits Survey, the average annual premium for employer-sponsored family health coverage is approaching $27,000, while single coverage averages around $9,325. While employees typically contribute a portion of this premium, the employer’s share remains a substantial expense. As a reference point, California’s state employee health plans for 2025 show monthly premiums for single coverage ranging from approximately $820 to over $1,300, illustrating the significant cost even for individual plans.

- Paid Time Off (PTO): This is a direct labor cost that is frequently underestimated in financial planning. An employee with 20 days of vacation and sick leave, plus 8 paid public holidays, receives 28 days of pay without performing billable work. This equates to 224 hours in a standard 2,080-hour work year, meaning 10.8% of their salary is paid for non-productive time. This directly impacts their effective hourly cost and must be factored into calculations of their true billable rate.

- Retirement Contributions: A 401(k) plan with an employer match is a standard expectation for professional roles. A common matching formula (e.g., 50% of the employee’s contribution up to 6% of their salary) translates to an additional cost of up to 3% of the employee’s gross pay.

- Other Benefits: Additional benefits such as dental insurance, vision coverage, life insurance, and disability insurance further add to the total cost. While California’s Paid Family Leave (PFL) program is funded through the State Disability Insurance (SDI) tax, which is paid by the employee (1.2% of wages), it is still a critical part of the total compensation discussion when evaluating the attractiveness of an employment offer.

Step 3: Overhead and Ancillary Costs (The Hidden Multipliers)

Beyond taxes and benefits, a range of ancillary and overhead costs are required to recruit, onboard, and support an employee. These expenses must be allocated on a per-employee basis to arrive at a complete TCC.

- Recruitment and Onboarding: The process of finding and hiring a new employee is costly. The Society for Human Resource Management (SHRM) estimates the average cost-per-hire to be approximately $4,700. This includes expenses for job postings, recruiter time, and background checks. Once hired, the onboarding process can cost an additional $1,000 to $5,000 per employee, factoring in administrative time, formal training programs, and the initial period of reduced productivity as the new hire ramps up.

- Equipment and Workspace: Every employee requires a set of tools to perform their job. This includes the cost of a computer, monitors, software licenses, and other necessary hardware. Furthermore, if the employee works in an office, a portion of the facility’s rent, utilities, and office supplies must be allocated to them.

- Training and Development: To maintain a skilled and competitive workforce, ongoing investment in professional development is necessary. This typically amounts to 1-3% of an organization’s total payroll annually.

To crystallize these components into a tangible figure, the following table provides a line-item breakdown of the fully loaded annual cost for a hypothetical Marketing Manager in California with a base salary of $84,000 per year ($7,000 per month).

Table 1: Fully Loaded Annual Cost of a Full-Time Employee (California Marketing Manager Example)

| Cost Component | Calculation Basis | Annual Cost |

|---|---|---|

| Base Salary | — | $84,000.00 |

| Social Security | 6.2% of $84,000 | $5,208.00 |

| Medicare | 1.45% of $84,000 | $1,218.00 |

| FUTA | 0.6% of first $7,000 | $42.00 |

| California SUI | 3.4% of first $7,000 | $238.00 |

| California ETT | 0.1% of first $7,000 | $7.00 |

| Workers’ Compensation | 1.2% of $84,000 (low-risk role) | $1,008.00 |

| Subtotal: Mandatory Costs | $7,721.00 | |

| Health Insurance | $800/month employer contribution | $9,600.00 |

| Dental & Vision Insurance | $100/month employer contribution | $1,200.00 |

| Retirement Plan | 3% of salary (401k match) | $2,520.00 |

| Subtotal: Benefits | $13,320.00 | |

| PTO & Holidays (28 days) | ($84,000 / 260 workdays) * 28 days | $9,138.46 |

| Subtotal: Time-Off Cost | $9,138.46 | |

| Recruitment Cost | $4,700 amortized over 3 years | $1,566.67 |

| Onboarding & Training | $3,000 (1st year) + 1.5% of salary (ongoing) | $2,260.00 |

| Equipment & Software | $2,500 initial + $1,000/year | $1,833.33 |

| Office Space & Utilities | $400/month allocated cost | $4,800.00 |

| Subtotal: Ancillary & Overhead | $10,460.00 | |

| Total Annual Cost (TCC) | Sum of all costs | $124,639.46 |

| Final Cost Multiplier | TCC / Base Salary | 1.48x |

This detailed calculation demonstrates that the “1.25 to 1.4 times salary” rule of thumb can, in fact, be conservative. In this realistic scenario for a professional role in a high-cost state like California, the true cost to the company is nearly 1.5 times the employee’s base salary. This calculated, defensible number provides the necessary baseline for an accurate comparison with the freelancer model. For additional context, review how different accounting methods can affect how you see these expenditures in your financial statements.

II. The Freelancer Financial Model: Translating Rates into True Project Cost

Engaging freelancers offers a fundamentally different cost structure, one that shifts a significant portion of labor expense from a fixed to a variable category. However, a common mistake in financial analysis is to assume that a freelancer’s quoted rate represents their total cost. Freelancers are not simply “cheaper”; their pricing is structured to cover the very costs—taxes, benefits, equipment, and non-billable administrative time—that an employer covers for an FTE. A rigorous analysis requires translating their rates into a true, “all-in” project cost by accounting for the internal resources required to manage them effectively.

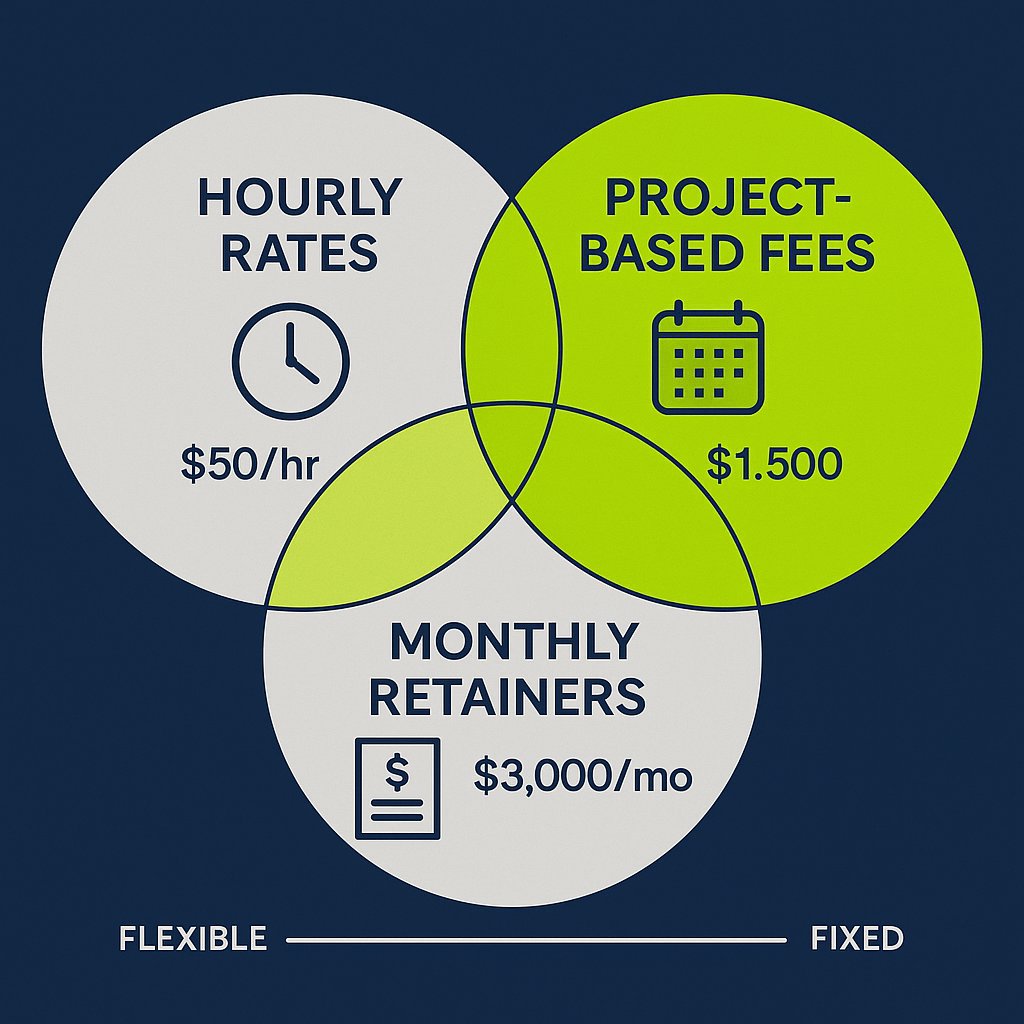

Understanding Freelancer Pricing Structures

- Hourly Rates: This is the most direct pricing model, where the agency pays for the time spent on a task. Rates for marketing and creative roles vary significantly based on experience, specialization, and geographic market. A general breakdown for 2025 shows:

- Entry-Level (0-2 years): $25 – $50 per hour.

- Mid-Level (2-5 years): $50 – $120 per hour.

- Expert (5+ years): $120+ per hour, with highly specialized consultants commanding significantly more. For instance, a freelance Digital Marketing Consultant averages around $82 per hour, while a Market Research specialist may charge $77 per hour.

- Project-Based Fees: This model provides cost certainty for the client by establishing a flat fee for a well-defined scope of work. This shifts the risk of inefficiency from the agency to the freelancer. Examples include a $3,000 fee for a website copywriting project or a $7,500 fee for a three-month SEO campaign. This model allows an agency to perfectly align a specific cost with a specific revenue stream, creating highly predictable project-level margins.

- Monthly Retainers: For ongoing needs, a monthly retainer ensures consistent access to a freelancer’s services for a fixed fee. This model is common for services like social media management, content marketing, or SEO maintenance. Retainers can range from $1,000 per month for basic services to over $10,000 per month for comprehensive, strategic support. This structure offers a middle ground between the variability of hourly work and the fixed commitment of an FTE, creating predictable monthly costs that can be more easily integrated into financial forecasts. The optionality provided by these different pricing models is a strategic tool for a CFO, enabling the construction of a more flexible and resilient cost structure that improves cash flow management. If you’re interested in how agencies address the challenges of in-house vs. outsourced accounting, see our comparison of accounting outsourcing models.

Calculating the “All-In” Freelancer Cost

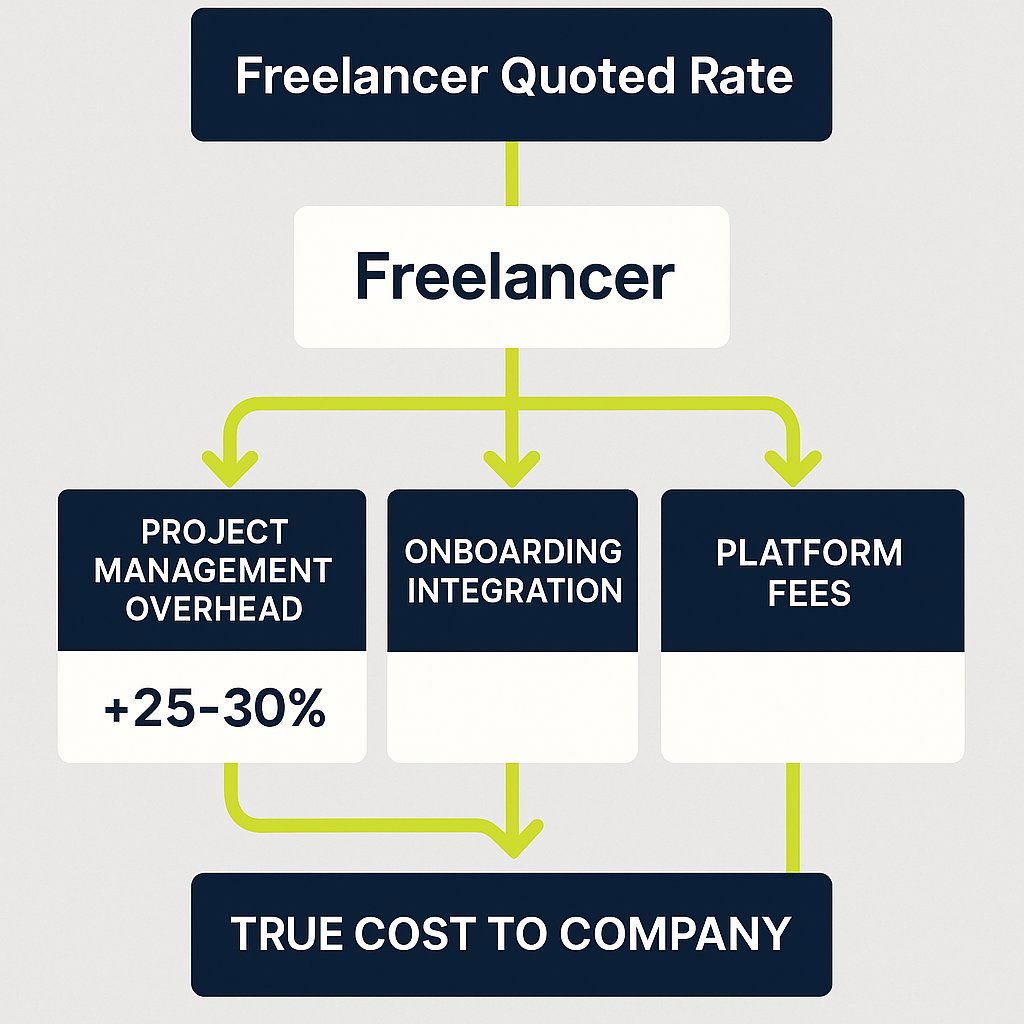

The freelancer’s invoice is only part of the total cost equation. To create a true “apples-to-apples” comparison with an FTE’s fully loaded cost, the agency must quantify and add the internal costs associated with managing that external resource.

- The Project Management (PM) Overhead: This is the most critical, and most frequently overlooked, indirect cost of using freelancers. An agency’s full-time staff must invest time in sourcing, vetting, briefing, managing, providing feedback, and integrating the freelancer’s work into the final client deliverable. This internal time is not free. A key industry guideline for maintaining profitability suggests that an agency should add a markup of 25-30% to a freelancer’s direct cost to account for this internal project management and client service time. This PM overhead is a necessary component of the true cost calculation.

- Onboarding and Integration Costs: While significantly less intensive than for an FTE, there is still a non-zero cost associated with bringing a new freelancer into the fold. This includes the time spent on contract negotiation, system access setup (e.g., to project management software or communication channels), and initial briefing on agency standards and client-specific requirements.

- Platform Fees: When sourcing talent through freelance platforms like Upwork or Fiverr, the agency must account for service or commission fees. These fees can range from 5% to 20% of the transaction value. Often, experienced freelancers will build this platform fee into their quoted rate, meaning the agency ultimately bears the cost.

This leads to a crucial concept for accurate financial comparison: the ‘Freelancer Burden Rate’. Just as an FTE’s salary is augmented by a “burden rate” of taxes and benefits, a freelancer’s quoted rate must be augmented by an internal “burden rate” of management and integration costs. A simple comparison of a freelancer’s $100 per hour rate to an FTE’s salary-derived hourly rate is a dangerously misleading oversimplification. By applying the 25-30% PM overhead guideline, that $100 per hour freelancer effectively costs the agency $125-$130 per hour in total allocated resources. This intellectually honest financial model prevents the chronic underestimation of the true cost of leveraging external talent. It fundamentally reframes the strategic question from “Who has a lower hourly rate?” to the more accurate and meaningful question, “What is the total cost to the company to complete this specific scope of work?”

III. The Profitability Matrix: A CFO’s Guide to Labor ROI

With a clear understanding of the true costs of both FTEs and freelancers, the analysis can now shift to the analytical core of the issue: how does the choice between them directly impact project and agency-level profitability? This requires moving beyond simple cost comparison to an examination of labor efficiency and its effect on the most critical metric for any service-based business. If you’ve ever wondered how time tracking supports not just project delivery, but your firm’s financial results and decision-making, explore our guide on strategic time tracking for agencies.

Introducing Gross Margin

For a service business where the “cost of goods sold” is primarily the cost of the people delivering the service, the single most important profitability metric is Gross Margin. It is a direct measure of how efficiently the agency converts revenue into profit before accounting for overhead (sales, general, and administrative expenses). It is calculated as:

Gross Margin = Agency Net Revenue – Direct Expenses / Agency Net Revenue

Where Agency Net Revenue is total revenue minus any pass-through costs (like ad spend or printing), and Direct Expenses are the direct costs of the people and tools required to fulfill the client work. This is where both the fully loaded cost of FTEs and the all-in cost of freelancers reside. A healthy, sustainable agency should target an overall Gross Margin of 50% or higher. To achieve this agency-wide goal, individual project margins must be even higher, ideally in the 60-70% range, to ensure there is sufficient gross profit to cover overhead and still yield a healthy net profit.

The Foundational Rules of Agency Profitability

To consistently achieve these target margins, two foundational pricing and costing rules are essential:

- The Freelancer 2x Rule: To maintain a healthy 50% Gross Margin on work performed by a freelancer, the agency must charge the end client at least double what it pays the freelancer. For example, if a freelancer is paid $5,000 for a project component, the agency must bill the client at least $10,000 for that same component.

- The Employee 3x-4x Rule: An employee’s billable work must generate revenue that is three to four times their direct salary cost. This larger multiplier is necessary to cover not only their salary but also their fully loaded cost (the ~1.5x TCC calculated earlier) and their share of agency overhead, while also accounting for the fact that they are not 100% billable.

Utilization Rate: The Great Equalizer

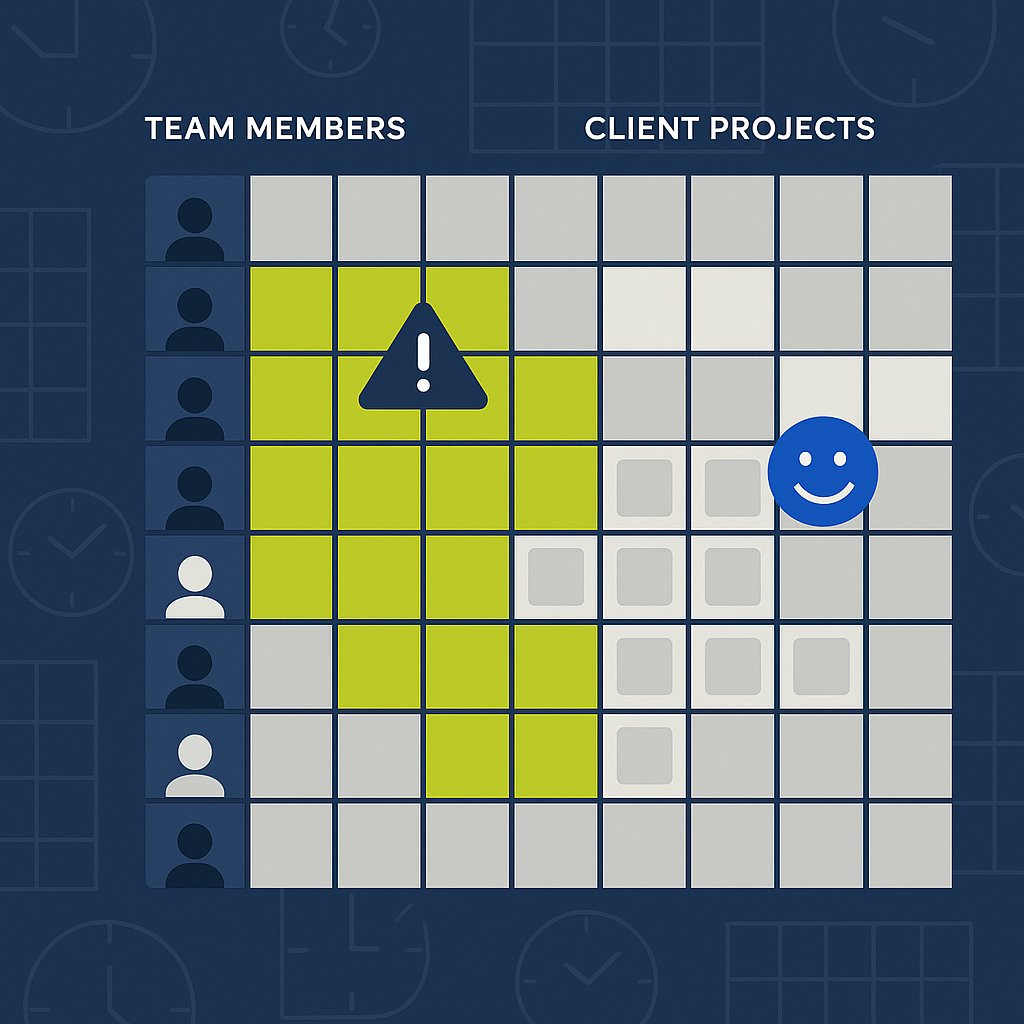

The concept of non-billable time leads directly to the most critical variable in comparing the profitability of FTEs and freelancers: the utilization rate. This metric is defined as the percentage of an employee’s total paid hours that are spent on direct, billable client work. Reaching a 100% utilization rate for an FTE is impossible. A significant portion of their time is consumed by non-billable (but necessary) activities such as internal meetings, administrative tasks, training, business development, and paid time off. A realistic and often ambitious target for a delivery-focused employee is a utilization rate of 70-80%. If untracked admin and non-billable time are draining your agency profits, read about how to stop the silent profit leak by making operational costs visible.

This stands in stark contrast to the freelancer model. When a freelancer is engaged for a specific project and bills on an hourly or project basis, they are, by definition, 100% utilized for the hours billed to that project. The agency pays only for productive, billable output. This fundamental difference in utilization is the primary reason why a higher-priced freelancer can often be significantly more profitable than a seemingly lower-cost full-time employee on a project-by-project basis.

To illustrate this, consider the FTE from Section I. Their fully loaded annual cost (TCC) was calculated to be $124,639.46. Based on a standard 2,080-hour work year, their fully loaded cost per hour is approximately $59.92. However, this is their cost for every hour the agency pays for, whether billable or not. If that employee has a billable utilization rate of 70%, the agency’s true cost for each billable hour they produce is significantly higher. The calculation is:

Effective Cost per Billable Hour = Fully Loaded Cost per Hour / Utilization Rate

This $85.60 figure is the correct number to use when calculating project-level profitability for work done by this FTE. It represents the true cost to the agency of getting one hour of billable work from this employee. When this is compared to a senior freelancer who charges $100 per hour, the cost difference is no longer as dramatic as a simple comparison of salary to the freelance rate would suggest. The gap has narrowed considerably because the freelancer’s rate has internalized their non-billable time, while the FTE’s cost of non-billable time is an expense borne by the agency.

The following table provides a tangible, numerical demonstration of this dynamic, modeling the profitability of a hypothetical project staffed by an FTE versus a freelancer.

Table 2: Comparative Profitability Analysis: FTE vs. Freelancer on a $50,000 Project

| Metric | Staffed by FTE | Staffed by Freelancer |

|---|---|---|

| Project Revenue | $50,000.00 | $50,000.00 |

| Required Billable Hours | 250 | 250 |

| Agency Billable Rate | $200.00/hour | $200.00/hour |

| Effective Cost per Billable Hour | $85.60 | $100.00 |

| Total Labor Cost for Project | $21,400.00 | $25,000.00 |

| Project Gross Profit | $28,600.00 | $25,000.00 |

| Project Gross Margin | 57.2% | 50.0% |

Analysis:

At first glance, the FTE appears to be the more profitable option for this specific project, yielding a higher Gross Margin of 57.2% compared to the freelancer’s 50.0%. However, this analysis is incomplete without considering the broader context. The freelancer model guarantees that 100% of the $25,000 labor cost is directly tied to this $50,000 revenue stream. The cost is incurred if and only if the project exists.

For the FTE, the agency still incurs the full cost of their un-utilized time. The 30% of their hours that are not billed to this project (or any other) represent a fixed, unrecoverable cost that drags down overall agency profitability. If there is not enough billable work to keep the FTE at their 70% utilization target, their effective cost per billable hour skyrockets, and agency profits suffer. The freelancer model completely eliminates the financial risk of paying for this “idle time.” Therefore, while an FTE might be more profitable on a fully utilized project, the freelancer presents a more resilient and less risky cost structure, particularly in an environment of fluctuating client demand.

IV. The Strategic Impact on Scalability and Cash Flow

The decision between FTEs and freelancers extends far beyond project-level profitability calculations. It has profound, second-order effects on an agency’s long-term financial strategy, fundamentally shaping its ability to scale, manage risk, and maintain healthy cash flow. By understanding these strategic implications, a CFO can architect a workforce that not only delivers work efficiently but also enhances the financial resilience and enterprise value of the business.

From Fixed to Variable Cost Structure

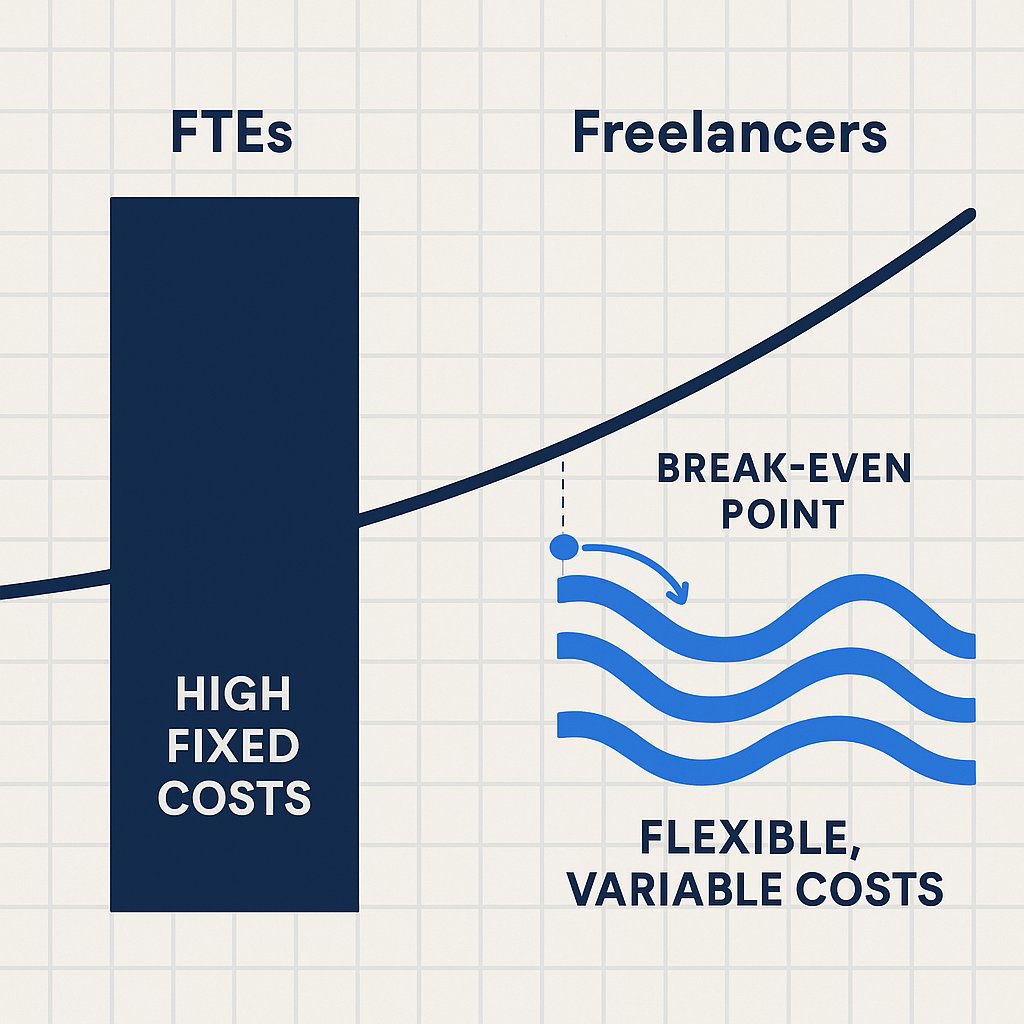

The most significant strategic difference between the two labor models lies in their impact on the agency’s operating leverage. Full-time employees, with their fixed salaries and benefits, represent a recurring, predictable cost on the profit and loss statement. This creates high operational leverage: when revenues are booming and the team is fully utilized, profits can grow at an accelerated rate. However, the inverse is also true. During economic downturns or periods of low client demand, these fixed costs persist, and losses can mount quickly.

Engaging freelancers fundamentally alters this dynamic. It allows an agency to transform a substantial portion of its largest expense category—labor—from a fixed cost into a variable cost. The cost of a freelancer is incurred only when there is revenue-generating work to be done. This direct linkage of expense to revenue is a powerful de-risking strategy, lowering the agency’s break-even point and creating a more durable financial model that is less susceptible to the natural ebbs and flows of project-based work.

Enhancing Scalability and Agility

This flexible cost structure is the engine of strategic agility and scalability. A workforce model that strategically blends a core team of FTEs with a network of on-demand freelancers provides the ability to rapidly adjust capacity in response to market opportunities and challenges.

- Scaling Up: A blended model empowers an agency to pursue and win large projects or onboard multiple new clients without the significant delay and long-term financial commitment inherent in the traditional FTE hiring process. The typical recruitment cycle for a full-time employee can be lengthy, whereas a trusted freelancer can often be engaged and start contributing within days. This model also provides immediate access to highly specialized skills—such as a GDPR compliance consultant, a mobile app developer, or a technical SEO specialist—that may be critical for a specific project but are not required on an ongoing basis, making a full-time hire financially unjustifiable.

- Scaling Down: Inevitably, agencies face periods of reduced demand, whether due to the conclusion of a major project or a broader economic slowdown. An agency with a high fixed-cost base composed primarily of FTEs faces the painful and disruptive prospect of layoffs to align costs with reduced revenue. In contrast, a variable, freelancer-centric model allows for a natural and less traumatic scaling down of costs. As project work decreases, freelancer contracts conclude, and expenses automatically contract in line with revenue, preserving margins and protecting the core business.

The Profound Impact on Cash Flow

For any service-based business, cash flow is the ultimate measure of financial health. According to SCORE, a staggering 82% of small business failures are attributable to poor cash flow management. The composition of the workforce has a direct and material impact on an agency’s ability to manage its cash effectively. To see the full spectrum of how accurate, up-to-date data supports strong cash management and decision-making, see Accurate Data in Accounting.

- Predictability and Forecasting: While FTE salaries represent a predictable monthly cash outflow, which can simplify baseline expense forecasting, this predictability comes at the cost of flexibility. Freelancer payments, which are typically tied to project milestones or monthly retainers for specific deliverables, can be more closely aligned with project-based cash inflows. When payment terms with freelancers (e.g., Net 30) are managed in concert with client invoicing schedules (e.g., 50% upfront, 50% on completion), it is possible to create a more dynamic and responsive cash flow cycle.

- Protecting the Cash Cushion: By leveraging freelancers, an agency avoids the significant and immediate cash drain associated with the full-time employment model: bi-weekly salary payments, monthly health insurance premiums, payroll tax deposits, and upfront recruitment fees. This preserves the agency’s cash reserves, which are absolutely critical for weathering unexpected financial storms, such as a major client paying late or the sudden loss of an account. A model that relies on a lean core team augmented by a flexible network of freelancers protects the financial foundation of the company by minimizing its fixed cash burn rate.

Ultimately, a blended workforce model acts as a financial shock absorber. Agency revenue is inherently volatile and project-driven. A cost structure heavy with fixed FTE salaries creates a high break-even point; when revenue dips below this threshold, the agency begins to burn through its cash reserves at an alarming rate. By shifting a significant portion of labor costs to a variable model, the break-even point is lowered. Costs naturally recede as revenues decline, protecting profitability and, most importantly, preserving cash. This demonstrated ability to maintain financial stability during downturns makes the business fundamentally less risky. For investors, lenders, and potential acquirers, this resilience and predictable cash flow are highly valuable. Therefore, the strategic composition of the workforce is not merely an operational choice; it is a key driver of the company’s long-term financial health and its overall enterprise value.

V. A Decision Framework for Optimal Workforce Composition

The analysis has demonstrated that neither the FTE nor the freelancer model is universally superior. The optimal approach lies not in a binary choice, but in the strategic blending of both to create a workforce architecture that is resilient, scalable, and profitable. This final section synthesizes the report’s findings into an actionable framework, moving beyond a simple list of pros and cons to provide a strategic tool for the agency.

Recap of Key Decision Factors

The choice for any given role or task should be evaluated against a consistent set of criteria that balance financial, operational, and strategic considerations.

- Financial: The primary financial drivers are the comparison between the fully loaded cost of an FTE and the all-in project cost of a freelancer, and the subsequent impact on Gross Margin. A critical, often overlooked, financial factor is the cost of underutilization, which is borne entirely by the agency in the FTE model.

- Operational: Key operational factors include the level of control and supervision required. FTEs allow for greater direct oversight, whereas the legal definition of an independent contractor requires a degree of autonomy in how the work is performed. Additionally, the importance of team integration, cultural contribution, and the building of institutional knowledge are significant advantages of the FTE model.

- Strategic: The strategic dimension hinges on the nature of the work itself. Is it a core, ongoing function central to the agency’s value proposition, or is it a specialized, episodic need tied to a specific project? The decision must also align with the agency’s broader strategic goals regarding scalability, market agility, and risk management.

The Four Quadrants of Workforce Planning

Instead of viewing the decision as a simple “either/or” choice, it is more effective to map the needs of the business onto a spectrum of workforce solutions. This can be visualized as a four-quadrant model based on the nature of the required role or task.

- Quadrant 1: Core Functions (High Integration, Ongoing Need)

- Description: These are roles that are central to the agency’s identity, daily operations, and long-term strategy. Examples include Account Directors, Creative Directors, Heads of Departments, and key operational staff (e.g., finance, HR).

- Optimal Model: Full-Time Employee (FTE).

- Rationale: These positions require deep institutional knowledge, consistent availability for leadership and team management, and a strong alignment with the company’s culture and values. The stability and commitment of an FTE are paramount for these foundational roles.

- Quadrant 2: Specialized Expertise (Low Integration, Episodic Need)

- Description: This quadrant covers high-skill tasks that are critical for specific projects but are not required on a continuous, 40-hour-per-week basis. Examples include a technical SEO audit for a website launch, advanced data analytics for a research project, motion graphics for a single video campaign, or specialized legal consultation.

- Optimal Model: Freelancer (Project-Based).

- Rationale: This model provides access to world-class, niche talent without the prohibitive long-term cost of employing a high-salaried specialist who would be underutilized for much of the year. It is the most financially efficient way to inject high-value expertise precisely when and where it is needed.

- Quadrant 3: Scalable Production (Low Integration, Variable Need)

- Description: This includes production-oriented tasks where the volume of work fluctuates directly with client demand. Examples are content writing, routine graphic design, social media content creation, and pay-per-click (PPC) campaign management.

- Optimal Model: Freelancer (Retainer or Project-Based).

- Rationale: Using a flexible pool of freelance talent for these functions allows the agency to scale its delivery capacity up or down in direct proportion to its revenue pipeline. This perfectly aligns costs with revenue, protects margins, and avoids the significant financial drain of maintaining a “bench” of underutilized full-time production staff during slow periods.

- Quadrant 4: Strategic Growth Initiatives (High Integration, Project-Based Need)

- Description: This quadrant addresses the staffing needs for new, unproven initiatives, such as launching a new service line or expanding into a new market. The long-term, full-time need for a role is uncertain at the outset.

- Optimal Model: Hybrid (Contract-to-Hire).

- Rationale: This approach minimizes the initial financial risk. An agency can engage a senior professional on a long-term contract basis to pilot the initiative. This provides the necessary expertise and focus without the immediate commitment of a permanent hire. If the initiative proves successful and a continuous need is established, the contractor can then be converted to a full-time employee.

This quadrant-based approach reveals that the most financially sophisticated strategy is not a choice between FTEs and freelancers, but the intentional blending of both to create a tiered, “Core-and-Flex” labor structure. This model is built around a lean, highly-utilized core of full-time employees who manage strategy, client relationships, and core operations (Quadrant 1). This stable core is then augmented by a flexible, scalable periphery of freelance specialists and production talent that can be engaged as needed to meet fluctuating client demands (Quadrants 2 & 3). This hybrid model maximizes the distinct advantages of both employment types, creating an organization that is simultaneously stable at its core, agile at its edges, and financially efficient throughout. It is a structure designed to align costs with the natural, project-based rhythm of agency work.

To operationalize this strategy and ensure consistent decision-making across the organization, the following matrix can be used by all hiring managers.

Table 3: Strategic Hiring Decision Matrix

| Role Characteristic | Key Decision Questions | Optimal Hiring Model |

|---|---|---|

| Core Business Function | Is this role essential for daily operations and long-term strategy? Does it involve managing other employees? | FTE |

| Requires Deep Institutional Knowledge | Is deep understanding of company history, processes, and culture critical for success in this role? | FTE |

| Specialized, Episodic Skill | Is this a high-skill need for a specific, time-bound project? What is the cost of this role being underutilized? | Freelancer (Project) |

| Variable / Fluctuating Demand | Does the volume of this work change significantly from month to month based on client needs? | Freelancer (Retainer/Project) |

| New Service / Pilot Program | Is this a new initiative where the long-term, full-time need is not yet proven? What is the financial risk of a permanent hire if the initiative fails? | Contract-to-Hire |

| Need for High Control/Supervision | Does the task require constant oversight and adherence to specific internal processes? | FTE |

| Need for Rapid Scaling | Do we need to increase our capacity in this area quickly without a long recruitment cycle? | Freelancer (Retainer/Project) |

Conclusion: Building a Financially Resilient, Talent-First Agency

The analysis presented in this report leads to a clear and powerful set of conclusions. The traditional debate of freelancers versus full-time employees, when viewed through a rigorous financial lens, is revealed to be a false dichotomy. The true path to sustainable profitability and strategic agility lies not in choosing one model over the other, but in mastering the art of the blend.

The key takeaways from this investigation are threefold:

- The true cost of an employee is significantly higher than their base salary. A detailed, fully loaded cost analysis, accounting for taxes, benefits, and overhead, is non-negotiable for accurate financial planning. For a professional role in a state like California, this cost can approach 1.5 times the gross salary.

- Profitability hinges on managing the utilization gap. A freelancer’s cost is directly tied to billable output, effectively making them 100% utilized on a given project. An FTE’s cost includes a substantial portion of non-billable time, which must be covered by the margins on their productive hours. This dynamic means a higher-priced freelancer can often be the more profitable choice for discrete, project-based work.

- A flexible, variable cost structure is a profound strategic advantage. By transforming labor from a fixed to a variable expense, an agency can enhance its cash flow, reduce financial risk, and build a more scalable and resilient business model capable of thriving in a volatile market.

The final strategic recommendation is, therefore, the formal adoption of a “Core-and-Flex” workforce model. This model, guided by the principles and tools outlined in the Strategic Hiring Decision Matrix, will enable AURA to build a workforce that is both a competitive advantage in the marketplace and a cornerstone of its long-term financial health. By maintaining a lean, stable core of full-time strategic leaders and augmenting them with a flexible, on-demand network of specialized freelance talent, an agency can optimize its cost structure, protect its profitability, and position itself for sustainable, scalable growth. This is the future of agency finance: a talent-first approach built on a foundation of strategic financial resilience.

Transform Your Agency with Strategic Time Tracking in 2025

Why Does My Agency Need Time Tracking? A CFO’s Guide to Unlocking Profitability and Clarity

It’s a familiar story for agency owners. The team is swamped, new clients are signing on, and revenue is climbing. You’re busier than you’ve ever been. So why does cash flow still feel tight? Why doesn’t the bottom line reflect all the incredible work your team is shipping? If you’ve ever looked at your P&L statement and thought, “This doesn’t feel right,” you’re not alone. This is the agency owner’s dilemma: being busy, but not knowing if you’re truly profitable.

For many creative, marketing, and tech agencies, the mere mention of “time tracking” can trigger a collective groan. It’s often seen as a straightjacket on the fluid, non-linear creative process—an administrative burden that stifles innovation. To your team, it can feel like a tool for micromanagement, a way for “big brother” to watch their every move. And if you’re not billing by the hour, it can seem like a completely pointless exercise.

Let’s reframe the conversation.

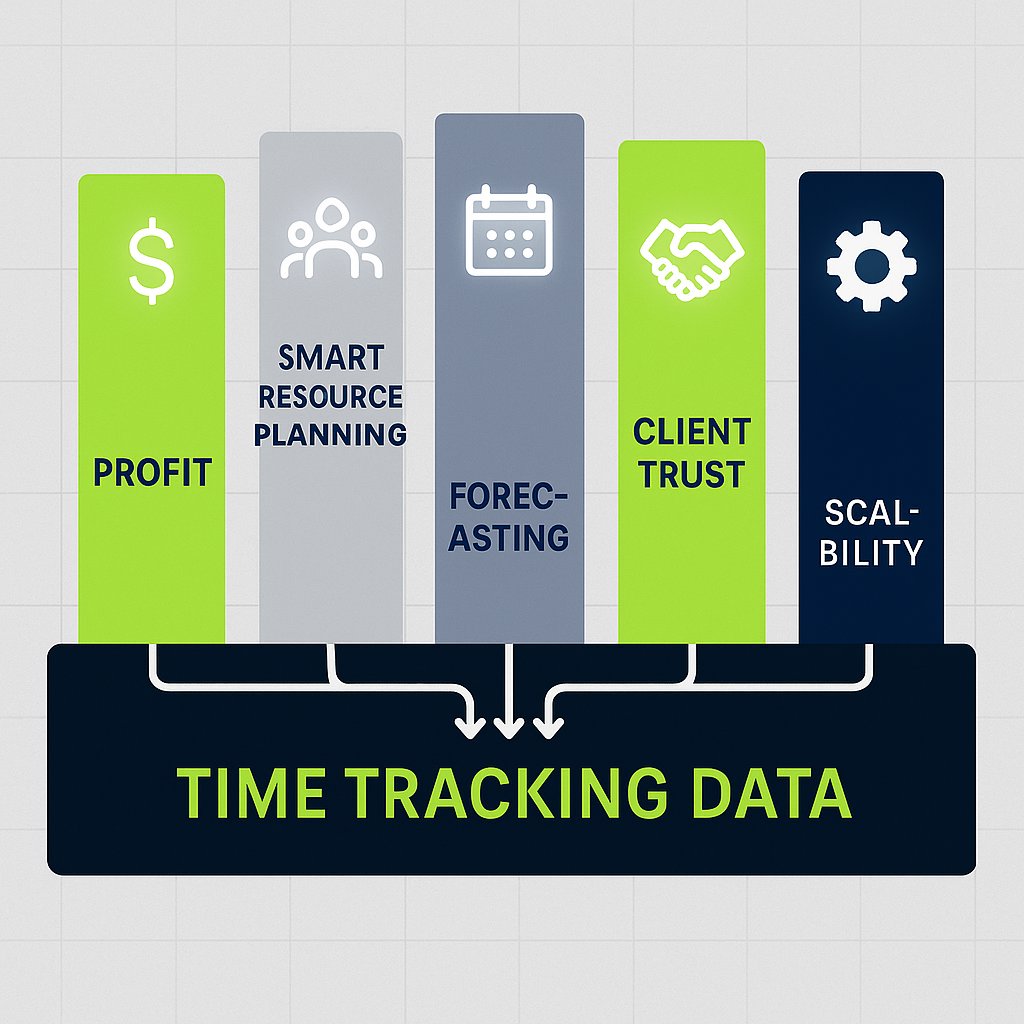

Effective time tracking is not about surveillance. It’s about intelligence. It is the single most critical source of business data your agency can have, transforming your leadership from reactive and gut-driven to proactive and strategic. It is the foundational layer for gaining the clarity, confidence, and control you need to scale profitably.

Often, the most painful issues in an agency—like team burnout, high employee turnover, and tense client relationships—are treated as HR or account management problems. But in reality, they are lagging indicators of a deeper financial and operational issue. The chain of events is clear: without historical data on how long projects actually take, scoping is guesswork. This guesswork leads to underpricing and a constant battle with scope creep, where extra revisions and requests slowly erode your margins. The result? An overworked, burnt-out team and a profitability problem that no amount of team-building can fix. Time tracking provides the objective data needed to solve the root cause, not just treat the symptoms.

Part I: The Strategic Shift—From Tracking Hours to Tracking Value

To truly understand the power of time tracking, you have to stop seeing it as an administrative task and start seeing it as a C-suite level strategic tool. It’s not about counting minutes; it’s about understanding the fundamental economics of your business.

Uncovering Your True Profitability: The Difference Between Revenue and Sanity

Top-line revenue is a vanity metric. It feels good to say you’re a “$3 million agency,” but if your expenses are $2.95 million, that number doesn’t mean much. Profit is what funds your growth, your team’s salaries, and your own sanity. Many agencies chase revenue growth while their profitability flatlines because they don’t have visibility into their biggest cost: their team’s time.

Time data is the only way to calculate the true profitability of every client, every project, and every service you offer. It allows you to calculate your “delivery margin”—the profit you generate from client work after the full cost of your team’s labor is accounted for. For example, a flashy $100,000 project that consumes 1,000 team hours might have a lower delivery margin than a less glamorous $80,000 project that only takes 500 hours. Without time data, you might be fighting to win more of the wrong kind of work.

Mastering Your Pricing and Scoping: From Guesswork to Confidence

Underpricing is one of the most common and destructive financial mistakes an agency can make. It often happens because, without data, you’re guessing what a project will cost to deliver. Time tracking is the antidote. Having a historical record of the actual hours your team spent on similar projects is the only way to build accurate, data-driven proposals that protect your margins from day one.

This data-backed confidence is also what empowers you to move away from hourly billing and toward more profitable value-based pricing models. When you know your true costs with certainty, you can price your services based on the immense value you deliver to the client, not the hours it takes to produce the work.

Furthermore, it gives you a powerful tool to combat scope creep. When a client asks for “just one more small revision,” you can move the conversation from subjective to objective. Instead of a difficult negotiation, it becomes a simple, data-informed statement: “We’d be happy to. The original scope included 15 hours for revisions, which we’ve used. Our data shows this next round will take approximately 5 additional hours. We can add that to the project for [cost].” This protects your team, your timeline, and your profitability.

Optimizing Your Most Valuable Asset: Your Team

For any agency, your single largest investment and expense is your people. Time tracking is the primary tool for managing that investment effectively. The data it generates provides a clear picture of resource allocation across the entire agency. It instantly reveals who is consistently over-utilized and at risk of burnout, and who is under-utilized, signaling a potential inefficiency or a need to fill the sales pipeline. This allows you to balance workloads intelligently, keeping your team healthy and productive.

This data also transforms performance reviews. Instead of relying solely on subjective feedback, you have objective metrics. You can see an employee’s efficiency, identify their most profitable skills, and find opportunities for professional development. For instance, you might discover a designer who is slower on logo projects but exceptionally fast and profitable when creating website mockups. This insight allows you to channel them toward their highest-value work, benefiting both the employee and the agency’s bottom line.

Part II: The Five Pillars of a Financially Healthy Agency

Implementing time tracking isn’t just about collecting data; it’s about building a stronger, more resilient, and more profitable business. The data you gather becomes the foundation for five essential pillars of agency health.

Pillar 1: Crystal-Clear Project & Client Profitability

A standard P&L statement gives you a blended, high-level view of your business. It can tell you if you were profitable last month, but it can’t tell you why. Was it because of Client A, or in spite of Client B? To make strategic decisions, you need granular data. By tracking time and understanding the “fully loaded cost” per employee (which includes salary, benefits, and a share of overhead), you can analyze every project with surgical precision.

This simple analysis can be revolutionary. It moves the invisible cost of your team’s time onto the balance sheet for each project, revealing which clients are fueling your growth and which are silently draining your resources. If you’re not sure your data is strong, accurate data in accounting is essential to give you confidence in your results.

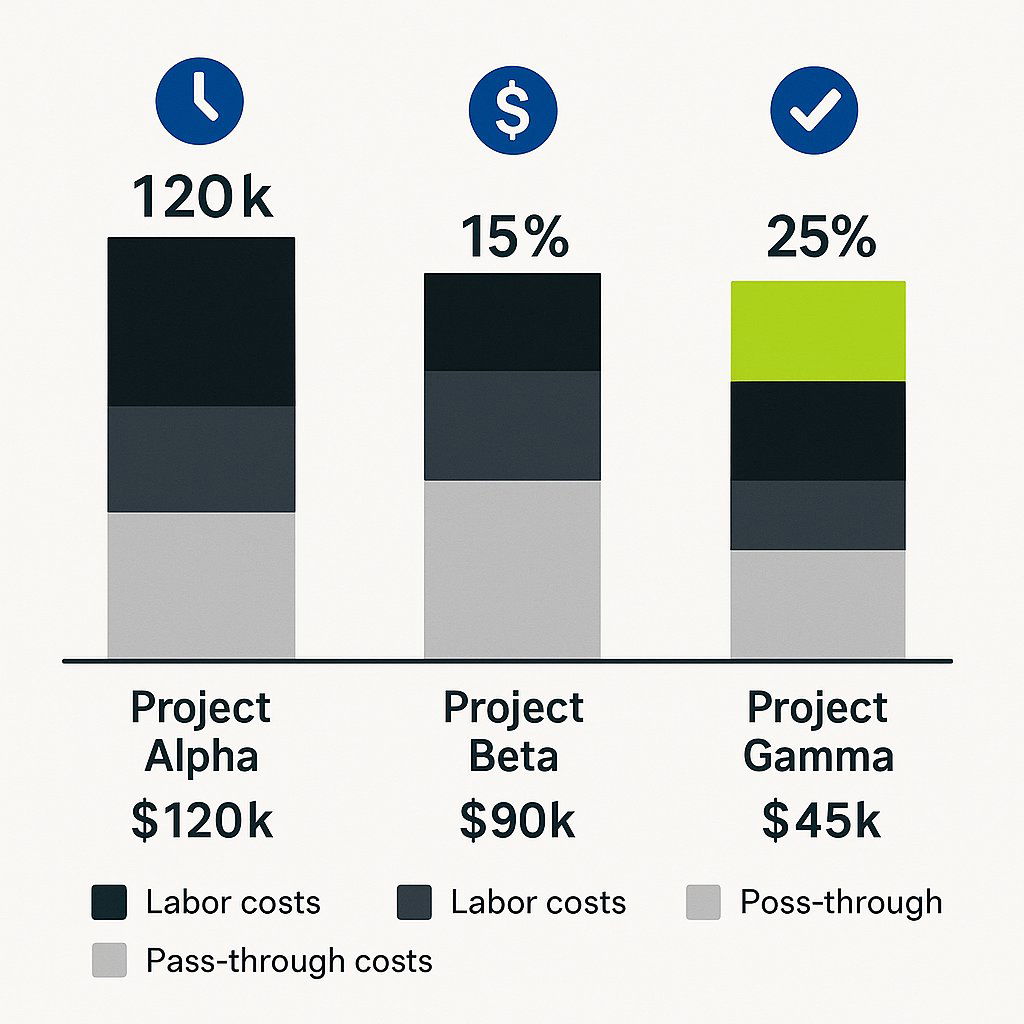

| Metric | Example Project A | Calculation Notes |

|---|---|---|

| Project Revenue | $50,000 | The total fee charged to the client. |

| Pass-Through Costs | ($5,000) | Ad spend, stock photos, contractor fees, etc. |

| Adjusted Gross Income (AGI) | $45,000 | Revenue - Pass-Through Costs |

| Total Hours Tracked | 410 hours | Sum of all team hours from your time tracking tool. |

| Avg. Fully Loaded Cost/Hour | $75/hr | Your agency’s average employee cost. |

| Total Labor Cost | ($30,750) | Total Hours Tracked * Avg. Cost/Hour |

| Net Profit | $14,250 | AGI - Total Labor Cost |

| Profit Margin | 31.7% | (Net Profit / AGI) * 100 |

Pillar 2: Data-Driven Resource & Capacity Planning

Without data, key decisions like hiring are often based on “feeling busy.” Time tracking replaces that feeling with facts. When you can see that your team is consistently operating at or above capacity on billable work, you know that a new hire is not just a cost, but an investment that the business can support and requires to grow.

This data is also crucial for capacity planning. By analyzing past projects, you can understand your team’s true capacity for work, which prevents you from over-promising and under-delivering to clients. It also informs the critical hire vs. outsource decision. If your data shows a consistent need for 15 hours per week of specialized copywriting, for example, it may be far more profitable to bring on a part-time employee than to continue paying a premium for freelancers.

Pillar 3: Accurate Forecasting & Predictable Cash Flow

The “feast or famine” cycle is a classic agency struggle, and it stems from a lack of predictability. When you know precisely how long your projects take and what your true profit margins are, you can forecast future revenue and expenses with a much higher degree of accuracy.

This predictability is a game-changer. It allows you to make strategic investments in new services, technology, or marketing with the confidence that you will have the cash flow to support them. It also provides the perfect tool for managing retainers. With time tracking, you can easily see if a client is consistently using more hours than their agreement covers, giving you clear, undeniable evidence to justify a conversation about increasing the retainer or scoping a new project—and to steer the business toward predictable cash flow over time.

Pillar 4: Radical Client Transparency & Trust

Many agencies view sharing time reports with clients as a defensive move, something you only do when an invoice is questioned. This is a missed opportunity. Proactively sharing simplified reports is a powerful way to build trust and strengthen relationships.

These reports demonstrate the immense value your team is delivering behind the scenes. They justify budgets and build client confidence, turning your relationship from a simple vendor transaction into a strategic partnership. The conversation shifts from “How much does this cost?” to “How can we best allocate our budget for maximum impact?” with you positioned as the trusted, data-informed advisor.

Pillar 5: A Scalable Operational Engine

Finally, time tracking is the key to building an agency that can grow without breaking. The data it generates is a spotlight that illuminates hidden inefficiencies and bottlenecks in your delivery process. Are you spending too much time on non-billable internal meetings? Does the QA phase of every web project take 50% longer than you estimated?

Answering these questions is the foundation of continuous improvement. By identifying and fixing these operational drags, you make your service delivery more efficient. For every fixed-fee project, that increased efficiency translates directly into higher profit margins. These refined, standardized, and data-proven processes create a scalable engine that allows your agency to take on more work without sacrificing quality or profitability.

Part III: The Implementation Playbook—Making Time Tracking Stick

Knowing why you need to track time is one thing; getting your team to do it consistently is another. Success depends less on the software you choose and more on the culture you build around it.

Step 1: Gaining Team Buy-In (It’s Not Big Brother)

The single biggest obstacle to successful time tracking is employee resistance, which is almost always rooted in the fear of being micromanaged. If your team believes the data will be used to punish them for taking “too long” on a task, they will either resist the process or fudge their numbers, making the data useless.

Therefore, the rollout must be framed as a tool for empowerment, not enforcement. The conversation should focus entirely on the benefits to the team. When introducing the initiative, use talking points that address their primary concerns:

- “This is our best tool to prevent burnout.” By making workloads visible, we can see who is overloaded and rebalance tasks before anyone gets overwhelmed.

- “This will help us set more realistic deadlines.” With accurate data, we can stop over-promising and create project timelines that are achievable without late nights and weekend work.

- “This data is how we justify hiring more people.” When we can prove we’re at capacity, it builds the business case for bringing in more help to support you.

- “This helps us recognize and reward your hard work.” Objective data on efficiency and profitability provides tangible evidence to support raises and promotions.

Crucially, leadership must lead by example. Track your own time and be transparent about what you’re learning. When the team sees that time data leads directly to a new hire that eases their workload, they will become your biggest advocates.

Step 2: Designing Your Framework & Choosing Your Tools

Don’t overcomplicate the setup. The goal is consistent adoption, not forensic-level detail. Start with a simple, logical framework that everyone can understand. A great starting point is:

- Level 1: Client

- Level 2: Project

- Level 3: Task/Service Line (e.g., Strategy, Design, Development, Project Management)

- Tag: Billable vs. Non-Billable

When choosing software, user-friendliness is the most important feature. The tool should be simple, intuitive, and feel seamless. Look for solutions that integrate directly with the project management tools your team already uses, like Asana, ClickUp, or Trello. This reduces friction by allowing them to track time without constantly switching tabs. Popular and effective tools for agencies include Harvest, Toggl, and Everhour.

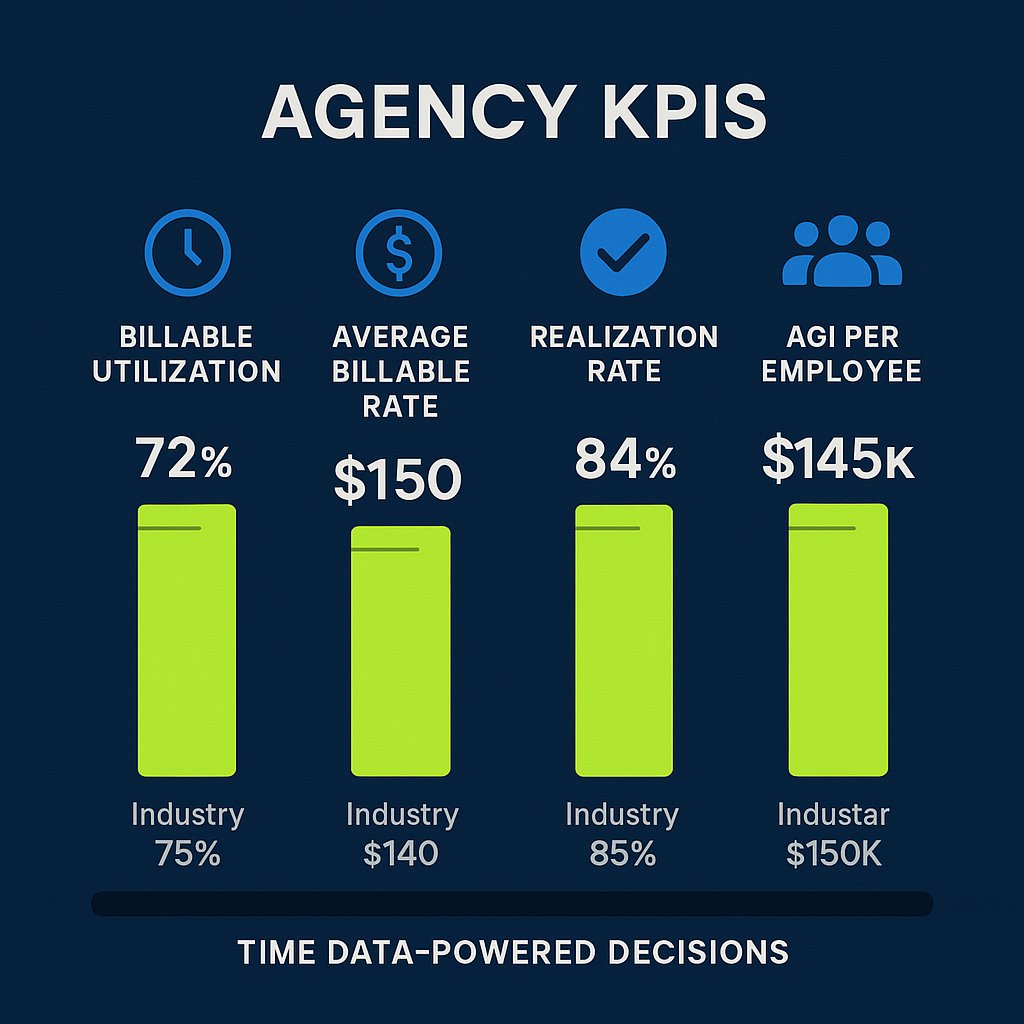

Step 3: From Data to Decisions—The KPIs That Matter

Collecting data is pointless if you don’t use it to make better decisions. By translating raw time data into a handful of Key Performance Indicators (KPIs), you can create a simple dashboard to monitor the health of your agency every month. And if you want to clarify the difference between finance roles, bookkeeper vs accountant vs controller vs CFO can help you understand how each position supports agency analytics and reporting.

| KPI | Formula | Industry Target | What It Reveals |

|---|---|---|---|

| Billable Utilization Rate | (Total Billable Hours / Total Capacity Hours) * 100 |

75-80% | Are we spending enough time on revenue-generating work? A low rate signals inefficiency or overstaffing. |

| Average Billable Rate (ABR) | Adjusted Gross Income / Total Hours Tracked |

Varies by agency | What is the effective hourly rate we earn? This helps identify your most profitable types of work. |

| Realization Rate | (Billed Hours / Billable Hours) * 100 |

>95% | Are we actually billing for all the billable work we do? A low rate indicates scope creep, write-offs, or over-servicing. |

| AGI per Employee | Total AGI / # of Full-Time Employees |

$150,000+ | Is our business model efficient? This is a key indicator of overall agency health and scalability. |

Conclusion: Your Agency’s New Compass

Time tracking is not just another task to add to your team’s plate. It is your agency’s compass. It provides the objective, reliable data you need to navigate the challenges of growth, pricing, and staffing. It gives you clarity on where your profits truly come from, the confidence to make bold strategic decisions, and ultimate control over your agency’s financial future.

Ready to take the first step? Don’t worry about buying and implementing a new tool just yet. This week, ask your team to track their time for a single project on a simple shared spreadsheet. At the end of the project, use the Project Profitability Analysis template from this article to see what the data tells you. The insights will likely surprise you—and set you on the path to more predictable, profitable growth.

Gaining financial clarity is a journey. When you’re ready to turn these insights into a strategic financial plan for your agency, our team at AURA is here to help you read the map.

Citations

- Goodey, Ben. “The Financial Fog: 8 Signs Your Agency’s Underperforming.” Scoro, https://www.scoro.com/blog/agency-financial-mistakes/.

- Petitpas, Marcel. “Agency Time Tracking – The Right Way.” Parakeeto, 23 June 2025, https://parakeeto.com/blog/how-to-track-time-with-marcel-petipas-episode-42/.

- McLellan, Drew. “How to Manage Small Business Finances as an Agency Owner with Jason Blumer.” Agency Management Institute, https://agencymanagementinstitute.com/how-to-manage-small-business-finances/.

Understanding Financial Statements: A Detailed Guide for Marketing Agency Owners

Introduction: Why Financial Literacy is a Strategic Necessity for Agency Leaders

If you’re running a marketing or communications agency, chances are you didn’t start your business because you love reviewing financial statements. You’re a strategist, a storyteller, a brand builder. As such, your focus is on the work: campaign launches, client pitches, creative briefs, hiring decisions, and sometimes putting out fires. Financials often take a back seat, that is, until there’s a cash crunch or a tax surprise.

But here’s the truth: your agency’s financial statements aren’t just for your accountant. They are strategic business tools that provide clarity, inform growth decisions, and safeguard profitability. When used properly, they can help you make smarter decisions, avoid cash flow surprises, and spot early warning signs before they become real problems. Without them, you’re making decisions in the dark.

The reality is that agency owners are brilliant marketers who often feel lost when they look at their balance sheet or profit & loss statement. That’s normal, but it is also fixable. This guide is your comprehensive walkthrough of the three essential financial statements every agency leader must understand and how to use them to build a smarter, more profitable business.

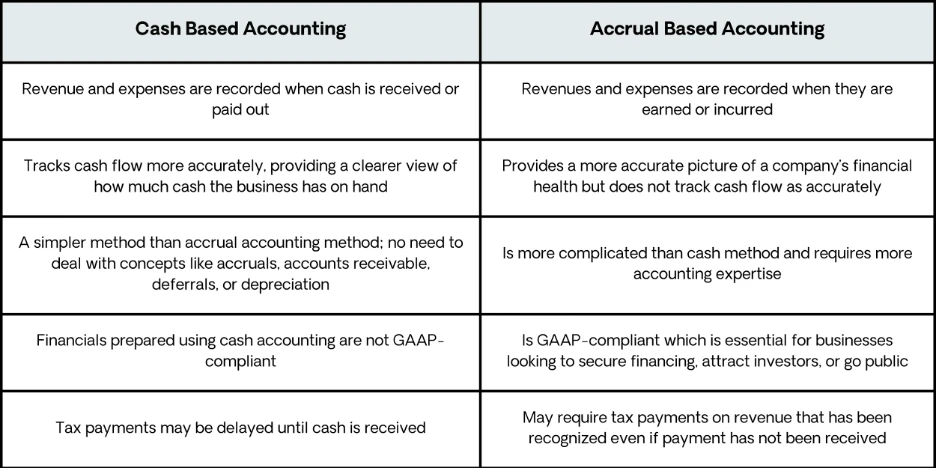

1. The Profit & Loss Statement (P&L): Your Agency’s Performance Barometer

What is it?

The Profit & Loss Statement, also called the Income Statement, tracks your agency’s revenues and expenses over a defined period, typically monthly, quarterly, or annually. It answers the simplest but most important question: is your agency making or losing money?

What it includes:

- Revenue – All income from client retainers, project work, consulting, and other services.

- Cost of Goods Sold (COGS) – Direct costs tied to producing client work and delivering services – subcontractor and freelance payments, ad spend, or media buys passed through.

- Gross Profit – Revenue minus COGS, which represents what’s left to pay your team and overhead.

- Operating Expenses – Salaries, software, rent, marketing, professional services, insurance, etc.

- Net Profit (or Loss) – Your “bottom line” – what’s left after all expenses are paid.

What marketing agency owners need to watch:

Gross Profit Margin

This shows how efficiently you’re delivering services, defined as a percentage of Gross Profit divided by Revenue. A healthy gross margin for an agency is typically 60–70% depending on your service mix.

Red Flag: If your gross margin is slipping, you may be underpricing, over-servicing, or carrying too many direct costs. This raises the question of whether you need to reclassify expenses or restructure delivery teams to restore healthy margins.

Operating Expense Ratios

High overhead can drown a profitable service model. Tools, subscriptions, and bloated team structures can quietly erode profits if not monitored regularly.

Net Profit Margin

Defined as Net Profit divided by Revenue, many marketing agencies operate at razor-thin margins or even losses without realizing it. A sustainable target should be 20% net profit after paying the owners market-rate salaries.

Why it matters:

The P&L shows whether your agency is operating profitably. More importantly, it helps you identify:

- Are your margins shrinking over time?

- Are your expenses growing faster than revenue?

- Are specific services or clients driving profit or dragging it down?

2. The Balance Sheet: Your Financial Health Snapshot

What is it?

The balance sheet gives you a point-in-time view of your agency’s financial position at a specific point in time. It tells you what your agency owns (assets), what you owe (liabilities) and what’s left over (equity or net worth). Think of it as your business’s financial pulse check.

What it includes:

- Assets – Cash, accounts receivable (invoices that you have sent to clients but have not yet been collected), prepaid expenses such as software, deposits and equipment.

- Liabilities – Credit cards, unpaid vendor bills, loans, deferred revenue.

- Equity – Owner investments, retained earnings and accumulated profits and losses.

Why it matters:

Cash Position

Is there enough cash in the bank to cover 1–2 months of operating expenses? If not, your agency is financially exposed, even if profitable.

Accounts Receivable (A/R)

How much money is owed to you? More importantly:

- Are clients paying on time?

- Are you offering terms that are too generous?

- Is your billing process causing delays?

Agencies with over 30% of revenue tied up in overdue receivables often face recurring cash flow problems. This normally triggers a need to build collection cadences and automated reminders to shorten cash cycles.

Debt Load

Carrying business loans or using credit lines is normal, but growth funded by excessive borrowing can cripple cash flow. If your liabilities are growing faster than assets, it’s time to pause and realign.

3. The Cash Flow Statement: Tracking Real Money Movement

What is it?

The P&L may show a profit, but that doesn’t mean you have money in the bank. That’s where the Cash Flow Statement comes in, tracking how cash enters and exits your business over a period of time.

This is often the most misunderstood and most important statement for agency owners.

Why? Because profit does not equal cash.

You can show $100,000 in profit on your P&L and still be unable to make payroll if you have not collected your client revenue and the cash has not yet hit your bank account.

What it includes:

- Operating Activities – Cash from day-to-day business operations, including client payments, payroll, rent, and vendor payments.

- Investing Activities – Equipment purchases, investments in new tools or systems (also called capital expenditures).

- Financing Activities – Owner distributions, new loans, and debt repayments.

Why it matters:

This statement helps you answer key questions like:

- Why am I profitable but still short on cash?

- Am I collecting payments fast enough to fund payroll?

- Is now a good time to make a major investment or should I wait?

How to use it strategically:

- Forecast cash needs 30–90 days out using a rolling forecast.

- Time investments or hiring based on available liquidity.

- Understand why your cash is decreasing even if profits look strong.

An example: An agency was showing $150k in profit but struggling to pay their freelancers. It turns out that the issue is related to a $200k spike in accounts receivable and a large upfront media spend that hadn’t yet been reimbursed. Building a rolling cash flow forecast that factors in client payment patterns, seasonal slowdowns, and major expenses will help agency owners identify gaps before they hit.

Common Mistakes Agency Owners Make with Financial Statements

Many agency owners fall into these traps:

- Confusing profit with cash – Remember, you can show profit and still be short of funds to be able to make your payroll.

- Ignoring balance sheet trends – A growing accounts receivable balance may be hiding deeper collection issues.

- Overlooking gross margins – Revenue growth is meaningless if you’re bleeding margin on delivery. Revenue is vanity and profit is sanity!

- Delegating too much without understanding – Bookkeepers and software can produce reports, but interpretation is where the strategic value lies.

Mistakes can be avoided by:

- Not relying solely on the P&L, as it is just one part of the puzzle. Your cash position completes the picture and gives you greater clarity of your numbers.

- Focusing on the balance sheet to understand whether your receivables balance or growing liabilities are undermining your business.

- Looking forward and not backwards. You should treat your financial statements as a roadmap used for planning.

- Being able to interpret your key numbers. Without understanding these figures, you are delegating one of your most critical leadership functions.

Best Practices for Agencies to Move from Confusion to Clarity

Financial statements serve agency owners best when they are turned into action. Understanding what they mean, identifying what needs attention, and implementing strategies to strengthen your financial position are all critical steps to going beyond the numbers.

- Understand the true profitability of services, clients, and projects.

- Spot trends and flag risks early using dashboards and forecasts.

- Improve internal processes for better financial hygiene.

- Turn data into action with monthly financial review meetings that drive strategic decision-making.

Financial Clarity Is a Competitive Advantage

Understanding your financial statements isn’t about becoming a numbers expert. It is about taking control of your agency’s future. If you’re serious about building a sustainable agency, one that’s not just busy but profitable, then you need to understand your numbers with enough fluency to make smart, timely decisions.

Your P&L tells you if you’re making money.

Your Balance Sheet shows what you’re worth.

Your Cash Flow Statement tells you whether you can keep going.

All three together are your business intelligence dashboard and your guide to building a smarter agency.

If you’re a marketing agency or professional services firm that is looking to scale, contact AURA today for a complimentary consultation.

Why Accurate Time Tracking Is Essential for Service-Based Businesses

Why it matters:

In service-based businesses, and especially in the marketing and communications-based industry, your offering is creativity, strategic thinking, and time. You are not selling widgets; you are selling brainpower. That makes time your most valuable (and expensive) resource.

Yet, time tracking remains one of the most overlooked and inconsistently executed practices among small to mid-sized agencies. Many agency heads and CEOs rely on ballpark estimates or outdated tracking systems, unaware of just how much money is lost when hours are inaccurately recorded, or worse, not tracked at all.

Excuses abound as to why staff don’t take time tracking seriously:

- It’s inconvenient

- Extra work takes staff away from delivering to the client

- It’s cumbersome to log in to software, which is often not intuitive

- The boss just wants to micromanage

- There is little to no understanding of why the business needs to track time in the first place

While you may have heard all of this, the fact remains that if you want to run a profitable, scalable service-based business, accurate time tracking isn’t a nice-to-have; it is non-negotiable.

Let’s explore why.

Time Tracking is the Backbone of Profitability

Starting with the basics: If you don’t know how much time it takes to execute a task, you cannot price it correctly. And if you can’t price it correctly, you’ll either overcharge and risk client attrition or undercharge and erode your margins, both of which are financially unsustainable.

Let’s say that your team is charging $10,000 for a brand identity project you estimate will take 80 hours; in reality, it takes 120 hours. That’s an extra 40 hours of unbilled time or 5 full workdays of lost revenue. Multiply that across 5 projects per year, and you’ve quickly absorbed $25,000 or more in unrecovered costs.

Now imagine if that was happening across multiple clients and service lines. Identifying this quickly highlights how time leakage eats away at the bottom line.

Enables Accurate Pricing and Project Scoping

One of the most common and potentially damaging habits we observe in agencies and other service-based businesses is “gut-based pricing”. You price a new project or assignment based on what you feel it’s worth or what you think the client will pay, without consulting the real data on delivery time.

Accurate time tracking transforms pricing from guesswork into a strategic approach.

By analyzing past projects, you gain clarity on:

- How long does it really take to complete deliverables (not what your team hopes)

- Where bottlenecks or inefficiencies occur

- What services consistently exceed time budgets

Armed with this information, you can develop pricing models that protect your margins and create more accurate project scopes, reducing creep and client disputes.

Clarifies Team Utilization and Prevents Burnout

Without detailed time tracking, it’s hard to know who’s truly at capacity, who’s underutilized, and how labor is distributed across billable and non-billable work.

Why this matters:

- In a marketing and service-based business, a benchmark utilization rate for employees should start at 80%

- This rate ensures that employees are spending most of their time on billable tasks while still having time for necessary non-billable activities like training, internal meetings and administrative tasks

- If you believe that a team member is fully utilized but they are not, you may end up making hiring decisions which cost the agency money or, miss revenue opportunities

Tracking time by client and project type reveals:

- How many hours are spent on revenue-generating work

- Which tasks are draining resources without adding value

- Whether you need to hire, outsource, or restructure your team

This data can also help set realistic internal expectations and prevent over-promising, which often leads to team fatigue.

Identifies Which Clients Are Profitable and Which Aren’t

Every agency has a “problem client”. They demand constant revisions, ignore scopes of work, and eat away at your team’s time. Unless you are accurately tracking time, you may not realize just how big of a problem or unprofitable this client is.

Time tracking allows you to evaluate client-level profitability, which means that you can:

- Compare hours worked vs. hours billed

- Identify which clients generate high-margin work

- Justify fees, rate increases or scope renegotiations

- Know when it is time to offload a low-value client

Having one client lose $10,000 per year due to over-servicing is one thing; having multiple clients lose this amount is a much bigger issue.

Improves Billing Transparency and Client Trust

Even if you do not bill hourly, time tracking supports clear communication, reporting and transparency.

Clients want to know they are getting value for their investment. When you have the data to support your deliverables, you

- Build transparency and trust

- Reduce billing disputes

- Make it easier to upsell new services based on demonstrated effort

And, if you bill by the hour, consistent time tracking is your only protection against scope-related disagreements and fee challenges.

Fosters a Culture of Accountability and Operational Excellence

As stated earlier, many team members resist time tracking. They feel that it is micromanagement or a lack of trust. But the issue isn’t the concept of time tracking; it is the culture around it.

When appropriately implemented, time tracking becomes a performance tool, not a punishment.

- It reveals where time is being lost to inefficiency

- It empowers team leads to better support their staff

- It supports goal setting, resource planning and bonus structures

Your team cannot improve what they cannot see. Time tracking gives them the visibility they need to make smarter decisions and helps leadership build stronger businesses.

How to Improve Your Time Tracking System

If your agency is still relying on end-of-week spreadsheets or Teams or Slack-type recaps, it’s time to reconsider. Implementing time tracking tools can simplify daily logging and help measure agency profitability metrics with greater precision.

Use the right tools:

There are many integrated platforms which exist, and you should research which system is right for your company.

Log time daily:

End-of-day or throughout the day logging increases accuracy and reduces time memory loss, where employees underestimate what they worked on

Track by project and task and not just by client:

The more granular your data, the more insightful your reporting

Educate and incentivize:

Explain the “why” behind time tracking to your team. Make it part of your culture and reward consistency and accuracy

A Financial Partner Can Help You Make Sense of It All

Having the proper financial partner will help analyze your time data alongside your financials to uncover insights like

- Which service lines are draining profitability

- When to hire vs. optimize

- Whether your pricing model supports your cost structure

- How to design a compensation model that aligns time with value

This analysis will help your agency move from busy to profitable.

Conclusion

Accurate time tracking isn’t about control; it’s about clarity.

It’s not a tool to monitor productivity; it’s a system to manage profitability.

If you’re not confident in where your agency’s time is going or whether it is being used profitably, you’re leaving money on the table.

Contact AURA today for a complimentary consultation and discover how we can identify the hidden time (and profit) in your business.

In-house Accounting vs. Outsourced Accounting: the Pros and Cons

A strong accounting infrastructure is crucial for the financial health of any business. Accurate, well-organized financial records give you a clear view of your company’s performance and the confidence to make strategic decisions that enable your company to scale. When it comes to ensuring the right accounting foundation is in place, business owners face a key choice: build an in-house accounting department or outsource your accounting functions. Each approach comes with unique advantages and challenges, and determining the best fit depends on a number of factors including your company’s size, industry, budget, and long-term growth objectives.

In this post, we’ll break down the pros and cons of an in-house versus an outsourced accounting solution so you can make an informed decision that aligns with your business strategy and long-term goals. Whether you’re seeking cost efficiency, specialized expertise, or more control over financial operations, we’ve got the insights to guide you to the decision that’s right for your business.

When is the Right Time to Hire an Accountant?

An accounting team has a wide range of important responsibilities within an organization. From overseeing your company’s financial systems and ensuring tax compliance to preparing financial statements, accounting is instrumental in developing, monitoring, and managing the company’s budgets and cash flow.

Generally, a business is ready for an accountant when their financial operations become more complex and require detailed reporting, analysis, and accurate, timely financial statements. A good accountant has in-depth knowledge of accounting standards, tax laws and regulations, and is proficient in accounting software and spreadsheets.

For detailed insights on the qualifications to look for in an accounting resource, check out our Comprehensive Guide for Businesses post which covers the different financial roles your company may need at various stages of its growth and how to choose the right expertise at the right time.

What is In-House Accounting?

In-house accounting involves hiring and training accountants to handle the company’s financial tasks, such as bookkeeping, generating financial statements, and tax preparation. In-house accounting is the traditional way of handling a company’s finances, where the accounting team is an integrated part of the organization rather than an external firm. By keeping accounting in-house, businesses can maintain direct control over their financial data and processes, ensuring that all financial operations align closely with the company’s specific needs and goals.

What Are the Pros of In-house Accounting?

Managing your accounting functions internally with dedicated staff has several advantages for businesses. Below are the biggest benefits to keeping your accounting in-house.

- Control & Oversight: By managing your accounting functions in house, you have full visibility and control over your company’s financial processes. This allows for real-time adjustments and close monitoring of your financial data.

- Tailored Processes: An in-house accounting department gives you more flexibility over your processes and procedures so that they can align with the specific needs of your business.

- Immediate Availability: An in-house accounting department means that you have a team readily available to answer questions, address urgent financial concerns, and collaborate directly with your leadership team and other departments.

- Cultural Alignment: Having your own accounting department means that your team members are more closely aligned with the company culture and strategic goals. This can result in better collaboration with other departments.

While in-house accounting offers control and oversight, it can also be expensive and require careful management. The financial implications of hiring full-time or part-time accountants, along with the potential quality variations and management challenges, need to be carefully considered.

What are the Cons of In-house Accounting?

Solely relying on in-house accountants can come with some drawbacks including the following:

- Limited Expertise: Smaller in-house accounting teams may lack the depth and specialization found in outsourced firms, potentially leading to gaps in knowledge. In addition, businesses that rely on a single in-house accounting resource can face delays and other issues if the employee is out of the office unexpectedly.

- Resource Constraints: During peak times like tax season or audits, in-house accounting staff may struggle with capacity, leading to potential burnout or errors.