Mastering Workforce Strategy in 2025: The CFO’s Guide

The CFO’s Strategic Guide to Workforce Composition: A Data-Driven Analysis of Freelancers vs. FTEs

Introduction: Beyond the Budget Line Item—Workforce as a Strategic Asset

The decision to hire a full-time employee (FTE) versus engaging a freelancer is one of the most critical financial levers an agency can pull. Historically viewed through a narrow lens of immediate cost savings, this choice is, in fact, a foundational element of financial strategy. It dictates the very nature of an organization’s cost structure, shaping its resilience, scalability, and long-term profitability. The composition of a workforce is not merely a line item on a budget; it is a strategic asset that determines an agency’s capacity to navigate market volatility, absorb economic shocks, and capitalize on growth opportunities. If you want to understand more about how agencies should approach their overall financials and accounting infrastructure, see our Accounting for Marketing Agencies: A Primer for a foundational overview.

For the modern Chief Financial Officer, the dilemma is acute. On one hand, full-time employees offer stability, cultural integration, and deep institutional knowledge—invaluable assets for building a cohesive and reliable team. On the other hand, freelancers provide unparalleled flexibility, access to a global pool of specialized talent, and a variable cost model that aligns expenses directly with revenue generation. Navigating this tension requires moving beyond anecdotal evidence and gut-feel decisions. It demands a quantitative framework grounded in a granular understanding of true costs and their second-order effects on the financial health of the business.

This report provides that framework. It is designed to replace ambiguity with analysis, offering a data-driven methodology for making optimal workforce composition decisions. The analysis will proceed through five distinct stages:

- A deconstruction of the true, “fully loaded” cost of a full-time employee, moving far beyond base salary.

- A financial model of the “all-in” project cost of a freelancer, accounting for hidden management overhead.

- A direct analysis of how each labor model impacts project and agency-level profitability metrics.

- An examination of the strategic consequences for cash flow, risk management, and scalability.

- The presentation of a strategic decision matrix to guide optimal workforce planning for any given business need.

By the conclusion of this report, leaders will be equipped with a clear, defensible, and financially rigorous approach to building the most effective and profitable workforce for the future. For those leading agencies, understanding the role of accurate time tracking in service-based businesses is also essential, as labor is your most expensive and valuable resource.

I. The Anatomy of an Employee: Deconstructing the Fully Loaded Cost of an FTE

To make an informed comparison, it is imperative to first establish a precise financial baseline for the cost of a full-time employee. Gross salary represents only the visible tip of the iceberg; the true cost to the company (TCC), often referred to as the “fully loaded cost” or “labor burden,” includes a significant overlay of mandatory taxes, benefits, and overhead that can substantially increase the total expense. A widely used rule of thumb suggests that the TCC is typically 1.25 to 1.4 times the employee’s base salary. Data from the U.S. Bureau of Labor Statistics (BLS) corroborates this, indicating that in the private sector, benefits alone account for nearly 30% of an employee’s total compensation package. For accurate financial planning and a valid comparison against freelance alternatives, a detailed, line-item calculation is essential. If you find financial statements confusing or want to dive deeper, our detailed guide for agency owners can help clarify the numbers behind these cost models.

Step 1: Mandatory Employer-Paid Payroll Taxes (The Non-Negotiables)

These costs are legally mandated and represent the first layer of expense on top of gross wages. For an employer operating in California, these contributions are specific and substantial.

- Social Security: The employer is required to contribute 6.2% of an employee’s wages up to the annual Social Security wage base limit. For 2025, this cap is set at $176,100.

- Medicare: A contribution of 1.45% is required on all of an employee’s wages, with no upper limit or wage cap.

- Federal Unemployment Tax (FUTA): The standard FUTA tax rate is 6.0% on the first $7,000 of an employee’s annual wages. However, employers in states with compliant unemployment programs receive a credit of up to 5.4%, resulting in a net FUTA tax rate of 0.6%. This amounts to a maximum of $42 per employee per year.

- State Unemployment Insurance (SUI): This is a state-level tax, and in California, it is paid on the first $7,000 of an employee’s wages. The tax rate for new employers is 3.4% for the first two to three years of operation. For established employers, the rate can vary significantly, from 1.5% to 6.2%, depending on their employment history. For modeling purposes, the new employer rate of 3.4% provides a conservative baseline.

- Employment Training Tax (ETT): California employers are also subject to the ETT, which is 0.1% on the first $7,000 of wages, contributing to a state fund for worker training programs.

- Workers’ Compensation Insurance: This insurance provides benefits to employees who get injured or become ill from a work-related cause. Rates are highly dependent on the industry and the specific job classification’s risk profile. For low-risk professional roles, such as a marketing manager or software developer, a rate of approximately 1.2% of the gross salary is a reasonable estimate.

Step 2: The High Cost of Benefits (The Strategic Levers)

The benefits package is often the largest and most variable component of an employee’s TCC. While these costs are significant, they are also strategic investments in attracting and retaining top talent. The decision to offer a competitive benefits package is the primary factor that elevates an employee’s true cost from the lower end of the 1.25x multiplier toward the 1.4x range and beyond. While mandatory taxes add a predictable 8-10% to a salary, the benefits package can easily add another 15-30%. For a CFO, this means that the design of the benefits program is a primary lever for managing the overall labor burden.

- Health Insurance: This is a cornerstone of any competitive benefits package and a major financial commitment for the employer. According to the 2025 Employer Health Benefits Survey, the average annual premium for employer-sponsored family health coverage is approaching $27,000, while single coverage averages around $9,325. While employees typically contribute a portion of this premium, the employer’s share remains a substantial expense. As a reference point, California’s state employee health plans for 2025 show monthly premiums for single coverage ranging from approximately $820 to over $1,300, illustrating the significant cost even for individual plans.

- Paid Time Off (PTO): This is a direct labor cost that is frequently underestimated in financial planning. An employee with 20 days of vacation and sick leave, plus 8 paid public holidays, receives 28 days of pay without performing billable work. This equates to 224 hours in a standard 2,080-hour work year, meaning 10.8% of their salary is paid for non-productive time. This directly impacts their effective hourly cost and must be factored into calculations of their true billable rate.

- Retirement Contributions: A 401(k) plan with an employer match is a standard expectation for professional roles. A common matching formula (e.g., 50% of the employee’s contribution up to 6% of their salary) translates to an additional cost of up to 3% of the employee’s gross pay.

- Other Benefits: Additional benefits such as dental insurance, vision coverage, life insurance, and disability insurance further add to the total cost. While California’s Paid Family Leave (PFL) program is funded through the State Disability Insurance (SDI) tax, which is paid by the employee (1.2% of wages), it is still a critical part of the total compensation discussion when evaluating the attractiveness of an employment offer.

Step 3: Overhead and Ancillary Costs (The Hidden Multipliers)

Beyond taxes and benefits, a range of ancillary and overhead costs are required to recruit, onboard, and support an employee. These expenses must be allocated on a per-employee basis to arrive at a complete TCC.

- Recruitment and Onboarding: The process of finding and hiring a new employee is costly. The Society for Human Resource Management (SHRM) estimates the average cost-per-hire to be approximately $4,700. This includes expenses for job postings, recruiter time, and background checks. Once hired, the onboarding process can cost an additional $1,000 to $5,000 per employee, factoring in administrative time, formal training programs, and the initial period of reduced productivity as the new hire ramps up.

- Equipment and Workspace: Every employee requires a set of tools to perform their job. This includes the cost of a computer, monitors, software licenses, and other necessary hardware. Furthermore, if the employee works in an office, a portion of the facility’s rent, utilities, and office supplies must be allocated to them.

- Training and Development: To maintain a skilled and competitive workforce, ongoing investment in professional development is necessary. This typically amounts to 1-3% of an organization’s total payroll annually.

To crystallize these components into a tangible figure, the following table provides a line-item breakdown of the fully loaded annual cost for a hypothetical Marketing Manager in California with a base salary of $84,000 per year ($7,000 per month).

Table 1: Fully Loaded Annual Cost of a Full-Time Employee (California Marketing Manager Example)

| Cost Component | Calculation Basis | Annual Cost |

|---|---|---|

| Base Salary | — | $84,000.00 |

| Social Security | 6.2% of $84,000 | $5,208.00 |

| Medicare | 1.45% of $84,000 | $1,218.00 |

| FUTA | 0.6% of first $7,000 | $42.00 |

| California SUI | 3.4% of first $7,000 | $238.00 |

| California ETT | 0.1% of first $7,000 | $7.00 |

| Workers’ Compensation | 1.2% of $84,000 (low-risk role) | $1,008.00 |

| Subtotal: Mandatory Costs | $7,721.00 | |

| Health Insurance | $800/month employer contribution | $9,600.00 |

| Dental & Vision Insurance | $100/month employer contribution | $1,200.00 |

| Retirement Plan | 3% of salary (401k match) | $2,520.00 |

| Subtotal: Benefits | $13,320.00 | |

| PTO & Holidays (28 days) | ($84,000 / 260 workdays) * 28 days | $9,138.46 |

| Subtotal: Time-Off Cost | $9,138.46 | |

| Recruitment Cost | $4,700 amortized over 3 years | $1,566.67 |

| Onboarding & Training | $3,000 (1st year) + 1.5% of salary (ongoing) | $2,260.00 |

| Equipment & Software | $2,500 initial + $1,000/year | $1,833.33 |

| Office Space & Utilities | $400/month allocated cost | $4,800.00 |

| Subtotal: Ancillary & Overhead | $10,460.00 | |

| Total Annual Cost (TCC) | Sum of all costs | $124,639.46 |

| Final Cost Multiplier | TCC / Base Salary | 1.48x |

This detailed calculation demonstrates that the “1.25 to 1.4 times salary” rule of thumb can, in fact, be conservative. In this realistic scenario for a professional role in a high-cost state like California, the true cost to the company is nearly 1.5 times the employee’s base salary. This calculated, defensible number provides the necessary baseline for an accurate comparison with the freelancer model. For additional context, review how different accounting methods can affect how you see these expenditures in your financial statements.

II. The Freelancer Financial Model: Translating Rates into True Project Cost

Engaging freelancers offers a fundamentally different cost structure, one that shifts a significant portion of labor expense from a fixed to a variable category. However, a common mistake in financial analysis is to assume that a freelancer’s quoted rate represents their total cost. Freelancers are not simply “cheaper”; their pricing is structured to cover the very costs—taxes, benefits, equipment, and non-billable administrative time—that an employer covers for an FTE. A rigorous analysis requires translating their rates into a true, “all-in” project cost by accounting for the internal resources required to manage them effectively.

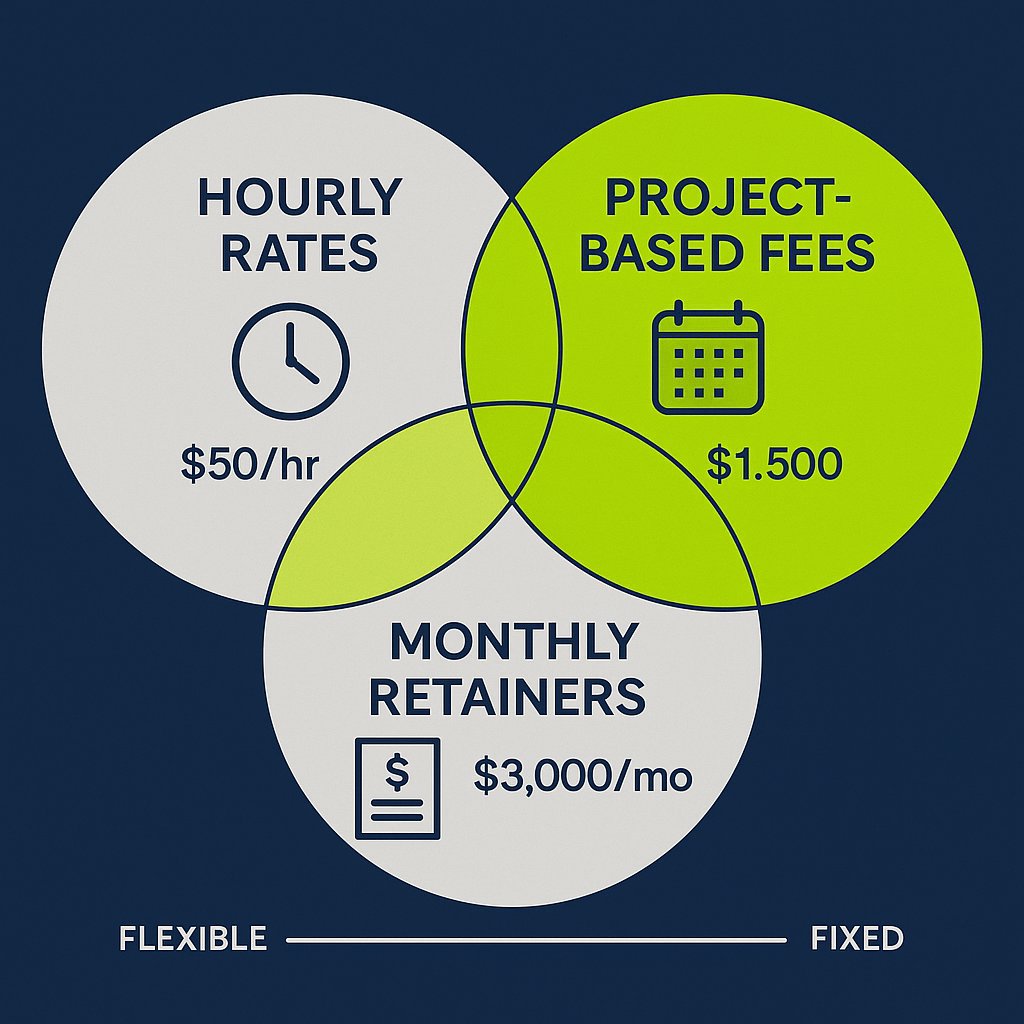

Understanding Freelancer Pricing Structures

- Hourly Rates: This is the most direct pricing model, where the agency pays for the time spent on a task. Rates for marketing and creative roles vary significantly based on experience, specialization, and geographic market. A general breakdown for 2025 shows:

- Entry-Level (0-2 years): $25 – $50 per hour.

- Mid-Level (2-5 years): $50 – $120 per hour.

- Expert (5+ years): $120+ per hour, with highly specialized consultants commanding significantly more. For instance, a freelance Digital Marketing Consultant averages around $82 per hour, while a Market Research specialist may charge $77 per hour.

- Project-Based Fees: This model provides cost certainty for the client by establishing a flat fee for a well-defined scope of work. This shifts the risk of inefficiency from the agency to the freelancer. Examples include a $3,000 fee for a website copywriting project or a $7,500 fee for a three-month SEO campaign. This model allows an agency to perfectly align a specific cost with a specific revenue stream, creating highly predictable project-level margins.

- Monthly Retainers: For ongoing needs, a monthly retainer ensures consistent access to a freelancer’s services for a fixed fee. This model is common for services like social media management, content marketing, or SEO maintenance. Retainers can range from $1,000 per month for basic services to over $10,000 per month for comprehensive, strategic support. This structure offers a middle ground between the variability of hourly work and the fixed commitment of an FTE, creating predictable monthly costs that can be more easily integrated into financial forecasts. The optionality provided by these different pricing models is a strategic tool for a CFO, enabling the construction of a more flexible and resilient cost structure that improves cash flow management. If you’re interested in how agencies address the challenges of in-house vs. outsourced accounting, see our comparison of accounting outsourcing models.

Calculating the “All-In” Freelancer Cost

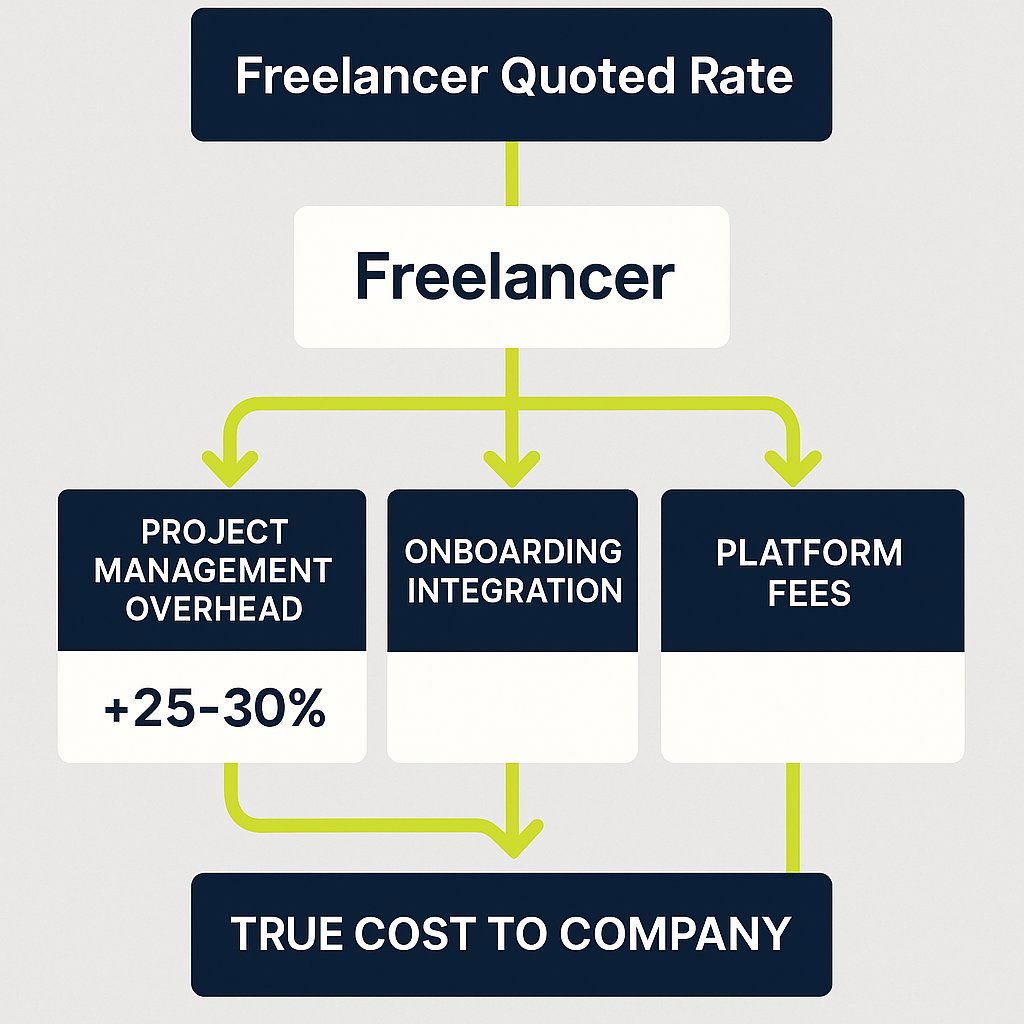

The freelancer’s invoice is only part of the total cost equation. To create a true “apples-to-apples” comparison with an FTE’s fully loaded cost, the agency must quantify and add the internal costs associated with managing that external resource.

- The Project Management (PM) Overhead: This is the most critical, and most frequently overlooked, indirect cost of using freelancers. An agency’s full-time staff must invest time in sourcing, vetting, briefing, managing, providing feedback, and integrating the freelancer’s work into the final client deliverable. This internal time is not free. A key industry guideline for maintaining profitability suggests that an agency should add a markup of 25-30% to a freelancer’s direct cost to account for this internal project management and client service time. This PM overhead is a necessary component of the true cost calculation.

- Onboarding and Integration Costs: While significantly less intensive than for an FTE, there is still a non-zero cost associated with bringing a new freelancer into the fold. This includes the time spent on contract negotiation, system access setup (e.g., to project management software or communication channels), and initial briefing on agency standards and client-specific requirements.

- Platform Fees: When sourcing talent through freelance platforms like Upwork or Fiverr, the agency must account for service or commission fees. These fees can range from 5% to 20% of the transaction value. Often, experienced freelancers will build this platform fee into their quoted rate, meaning the agency ultimately bears the cost.

This leads to a crucial concept for accurate financial comparison: the ‘Freelancer Burden Rate’. Just as an FTE’s salary is augmented by a “burden rate” of taxes and benefits, a freelancer’s quoted rate must be augmented by an internal “burden rate” of management and integration costs. A simple comparison of a freelancer’s $100 per hour rate to an FTE’s salary-derived hourly rate is a dangerously misleading oversimplification. By applying the 25-30% PM overhead guideline, that $100 per hour freelancer effectively costs the agency $125-$130 per hour in total allocated resources. This intellectually honest financial model prevents the chronic underestimation of the true cost of leveraging external talent. It fundamentally reframes the strategic question from “Who has a lower hourly rate?” to the more accurate and meaningful question, “What is the total cost to the company to complete this specific scope of work?”

III. The Profitability Matrix: A CFO’s Guide to Labor ROI

With a clear understanding of the true costs of both FTEs and freelancers, the analysis can now shift to the analytical core of the issue: how does the choice between them directly impact project and agency-level profitability? This requires moving beyond simple cost comparison to an examination of labor efficiency and its effect on the most critical metric for any service-based business. If you’ve ever wondered how time tracking supports not just project delivery, but your firm’s financial results and decision-making, explore our guide on strategic time tracking for agencies.

Introducing Gross Margin

For a service business where the “cost of goods sold” is primarily the cost of the people delivering the service, the single most important profitability metric is Gross Margin. It is a direct measure of how efficiently the agency converts revenue into profit before accounting for overhead (sales, general, and administrative expenses). It is calculated as:

Gross Margin = Agency Net Revenue – Direct Expenses / Agency Net Revenue

Where Agency Net Revenue is total revenue minus any pass-through costs (like ad spend or printing), and Direct Expenses are the direct costs of the people and tools required to fulfill the client work. This is where both the fully loaded cost of FTEs and the all-in cost of freelancers reside. A healthy, sustainable agency should target an overall Gross Margin of 50% or higher. To achieve this agency-wide goal, individual project margins must be even higher, ideally in the 60-70% range, to ensure there is sufficient gross profit to cover overhead and still yield a healthy net profit.

The Foundational Rules of Agency Profitability

To consistently achieve these target margins, two foundational pricing and costing rules are essential:

- The Freelancer 2x Rule: To maintain a healthy 50% Gross Margin on work performed by a freelancer, the agency must charge the end client at least double what it pays the freelancer. For example, if a freelancer is paid $5,000 for a project component, the agency must bill the client at least $10,000 for that same component.

- The Employee 3x-4x Rule: An employee’s billable work must generate revenue that is three to four times their direct salary cost. This larger multiplier is necessary to cover not only their salary but also their fully loaded cost (the ~1.5x TCC calculated earlier) and their share of agency overhead, while also accounting for the fact that they are not 100% billable.

Utilization Rate: The Great Equalizer

The concept of non-billable time leads directly to the most critical variable in comparing the profitability of FTEs and freelancers: the utilization rate. This metric is defined as the percentage of an employee’s total paid hours that are spent on direct, billable client work. Reaching a 100% utilization rate for an FTE is impossible. A significant portion of their time is consumed by non-billable (but necessary) activities such as internal meetings, administrative tasks, training, business development, and paid time off. A realistic and often ambitious target for a delivery-focused employee is a utilization rate of 70-80%. If untracked admin and non-billable time are draining your agency profits, read about how to stop the silent profit leak by making operational costs visible.

This stands in stark contrast to the freelancer model. When a freelancer is engaged for a specific project and bills on an hourly or project basis, they are, by definition, 100% utilized for the hours billed to that project. The agency pays only for productive, billable output. This fundamental difference in utilization is the primary reason why a higher-priced freelancer can often be significantly more profitable than a seemingly lower-cost full-time employee on a project-by-project basis.

To illustrate this, consider the FTE from Section I. Their fully loaded annual cost (TCC) was calculated to be $124,639.46. Based on a standard 2,080-hour work year, their fully loaded cost per hour is approximately $59.92. However, this is their cost for every hour the agency pays for, whether billable or not. If that employee has a billable utilization rate of 70%, the agency’s true cost for each billable hour they produce is significantly higher. The calculation is:

Effective Cost per Billable Hour = Fully Loaded Cost per Hour / Utilization Rate

This $85.60 figure is the correct number to use when calculating project-level profitability for work done by this FTE. It represents the true cost to the agency of getting one hour of billable work from this employee. When this is compared to a senior freelancer who charges $100 per hour, the cost difference is no longer as dramatic as a simple comparison of salary to the freelance rate would suggest. The gap has narrowed considerably because the freelancer’s rate has internalized their non-billable time, while the FTE’s cost of non-billable time is an expense borne by the agency.

The following table provides a tangible, numerical demonstration of this dynamic, modeling the profitability of a hypothetical project staffed by an FTE versus a freelancer.

Table 2: Comparative Profitability Analysis: FTE vs. Freelancer on a $50,000 Project

| Metric | Staffed by FTE | Staffed by Freelancer |

|---|---|---|

| Project Revenue | $50,000.00 | $50,000.00 |

| Required Billable Hours | 250 | 250 |

| Agency Billable Rate | $200.00/hour | $200.00/hour |

| Effective Cost per Billable Hour | $85.60 | $100.00 |

| Total Labor Cost for Project | $21,400.00 | $25,000.00 |

| Project Gross Profit | $28,600.00 | $25,000.00 |

| Project Gross Margin | 57.2% | 50.0% |

Analysis:

At first glance, the FTE appears to be the more profitable option for this specific project, yielding a higher Gross Margin of 57.2% compared to the freelancer’s 50.0%. However, this analysis is incomplete without considering the broader context. The freelancer model guarantees that 100% of the $25,000 labor cost is directly tied to this $50,000 revenue stream. The cost is incurred if and only if the project exists.

For the FTE, the agency still incurs the full cost of their un-utilized time. The 30% of their hours that are not billed to this project (or any other) represent a fixed, unrecoverable cost that drags down overall agency profitability. If there is not enough billable work to keep the FTE at their 70% utilization target, their effective cost per billable hour skyrockets, and agency profits suffer. The freelancer model completely eliminates the financial risk of paying for this “idle time.” Therefore, while an FTE might be more profitable on a fully utilized project, the freelancer presents a more resilient and less risky cost structure, particularly in an environment of fluctuating client demand.

IV. The Strategic Impact on Scalability and Cash Flow

The decision between FTEs and freelancers extends far beyond project-level profitability calculations. It has profound, second-order effects on an agency’s long-term financial strategy, fundamentally shaping its ability to scale, manage risk, and maintain healthy cash flow. By understanding these strategic implications, a CFO can architect a workforce that not only delivers work efficiently but also enhances the financial resilience and enterprise value of the business.

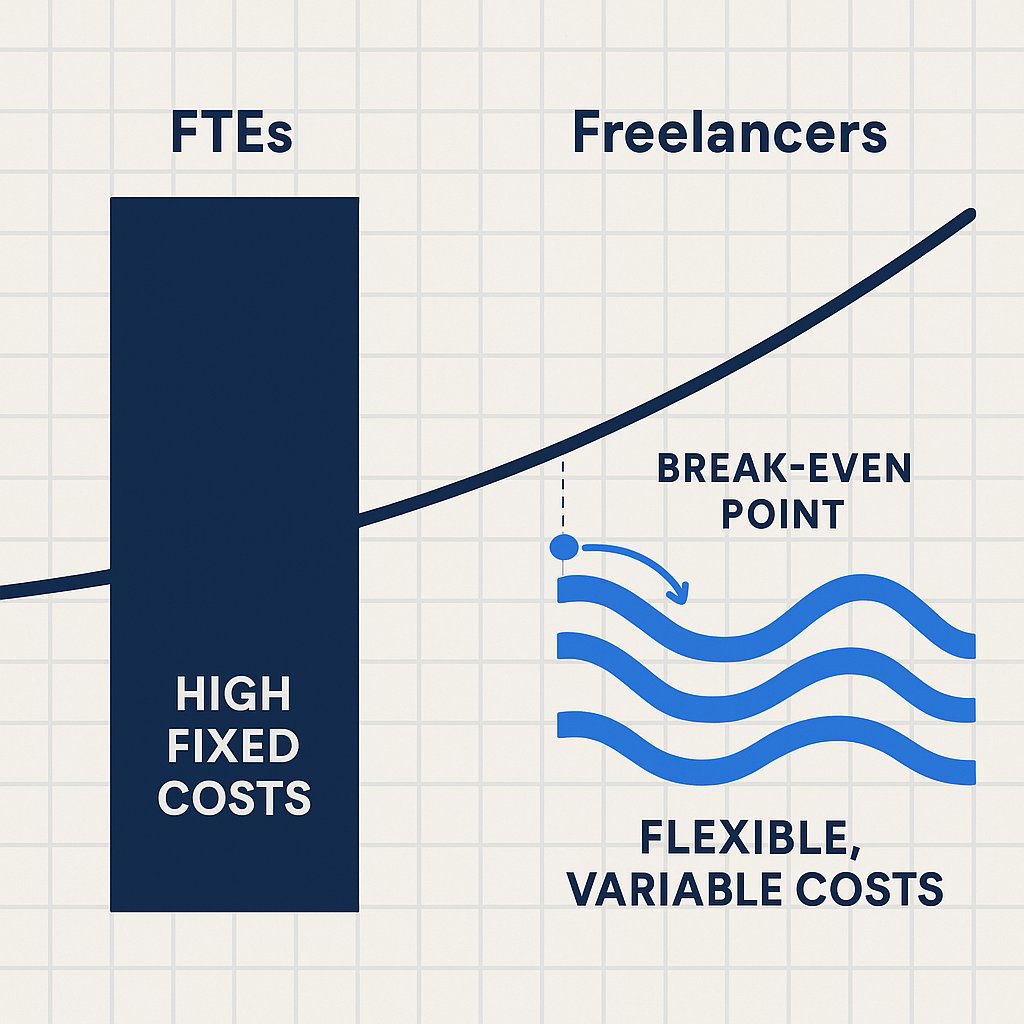

From Fixed to Variable Cost Structure

The most significant strategic difference between the two labor models lies in their impact on the agency’s operating leverage. Full-time employees, with their fixed salaries and benefits, represent a recurring, predictable cost on the profit and loss statement. This creates high operational leverage: when revenues are booming and the team is fully utilized, profits can grow at an accelerated rate. However, the inverse is also true. During economic downturns or periods of low client demand, these fixed costs persist, and losses can mount quickly.

Engaging freelancers fundamentally alters this dynamic. It allows an agency to transform a substantial portion of its largest expense category—labor—from a fixed cost into a variable cost. The cost of a freelancer is incurred only when there is revenue-generating work to be done. This direct linkage of expense to revenue is a powerful de-risking strategy, lowering the agency’s break-even point and creating a more durable financial model that is less susceptible to the natural ebbs and flows of project-based work.

Enhancing Scalability and Agility

This flexible cost structure is the engine of strategic agility and scalability. A workforce model that strategically blends a core team of FTEs with a network of on-demand freelancers provides the ability to rapidly adjust capacity in response to market opportunities and challenges.

- Scaling Up: A blended model empowers an agency to pursue and win large projects or onboard multiple new clients without the significant delay and long-term financial commitment inherent in the traditional FTE hiring process. The typical recruitment cycle for a full-time employee can be lengthy, whereas a trusted freelancer can often be engaged and start contributing within days. This model also provides immediate access to highly specialized skills—such as a GDPR compliance consultant, a mobile app developer, or a technical SEO specialist—that may be critical for a specific project but are not required on an ongoing basis, making a full-time hire financially unjustifiable.

- Scaling Down: Inevitably, agencies face periods of reduced demand, whether due to the conclusion of a major project or a broader economic slowdown. An agency with a high fixed-cost base composed primarily of FTEs faces the painful and disruptive prospect of layoffs to align costs with reduced revenue. In contrast, a variable, freelancer-centric model allows for a natural and less traumatic scaling down of costs. As project work decreases, freelancer contracts conclude, and expenses automatically contract in line with revenue, preserving margins and protecting the core business.

The Profound Impact on Cash Flow

For any service-based business, cash flow is the ultimate measure of financial health. According to SCORE, a staggering 82% of small business failures are attributable to poor cash flow management. The composition of the workforce has a direct and material impact on an agency’s ability to manage its cash effectively. To see the full spectrum of how accurate, up-to-date data supports strong cash management and decision-making, see Accurate Data in Accounting.

- Predictability and Forecasting: While FTE salaries represent a predictable monthly cash outflow, which can simplify baseline expense forecasting, this predictability comes at the cost of flexibility. Freelancer payments, which are typically tied to project milestones or monthly retainers for specific deliverables, can be more closely aligned with project-based cash inflows. When payment terms with freelancers (e.g., Net 30) are managed in concert with client invoicing schedules (e.g., 50% upfront, 50% on completion), it is possible to create a more dynamic and responsive cash flow cycle.

- Protecting the Cash Cushion: By leveraging freelancers, an agency avoids the significant and immediate cash drain associated with the full-time employment model: bi-weekly salary payments, monthly health insurance premiums, payroll tax deposits, and upfront recruitment fees. This preserves the agency’s cash reserves, which are absolutely critical for weathering unexpected financial storms, such as a major client paying late or the sudden loss of an account. A model that relies on a lean core team augmented by a flexible network of freelancers protects the financial foundation of the company by minimizing its fixed cash burn rate.

Ultimately, a blended workforce model acts as a financial shock absorber. Agency revenue is inherently volatile and project-driven. A cost structure heavy with fixed FTE salaries creates a high break-even point; when revenue dips below this threshold, the agency begins to burn through its cash reserves at an alarming rate. By shifting a significant portion of labor costs to a variable model, the break-even point is lowered. Costs naturally recede as revenues decline, protecting profitability and, most importantly, preserving cash. This demonstrated ability to maintain financial stability during downturns makes the business fundamentally less risky. For investors, lenders, and potential acquirers, this resilience and predictable cash flow are highly valuable. Therefore, the strategic composition of the workforce is not merely an operational choice; it is a key driver of the company’s long-term financial health and its overall enterprise value.

V. A Decision Framework for Optimal Workforce Composition

The analysis has demonstrated that neither the FTE nor the freelancer model is universally superior. The optimal approach lies not in a binary choice, but in the strategic blending of both to create a workforce architecture that is resilient, scalable, and profitable. This final section synthesizes the report’s findings into an actionable framework, moving beyond a simple list of pros and cons to provide a strategic tool for the agency.

Recap of Key Decision Factors

The choice for any given role or task should be evaluated against a consistent set of criteria that balance financial, operational, and strategic considerations.

- Financial: The primary financial drivers are the comparison between the fully loaded cost of an FTE and the all-in project cost of a freelancer, and the subsequent impact on Gross Margin. A critical, often overlooked, financial factor is the cost of underutilization, which is borne entirely by the agency in the FTE model.

- Operational: Key operational factors include the level of control and supervision required. FTEs allow for greater direct oversight, whereas the legal definition of an independent contractor requires a degree of autonomy in how the work is performed. Additionally, the importance of team integration, cultural contribution, and the building of institutional knowledge are significant advantages of the FTE model.

- Strategic: The strategic dimension hinges on the nature of the work itself. Is it a core, ongoing function central to the agency’s value proposition, or is it a specialized, episodic need tied to a specific project? The decision must also align with the agency’s broader strategic goals regarding scalability, market agility, and risk management.

The Four Quadrants of Workforce Planning

Instead of viewing the decision as a simple “either/or” choice, it is more effective to map the needs of the business onto a spectrum of workforce solutions. This can be visualized as a four-quadrant model based on the nature of the required role or task.

- Quadrant 1: Core Functions (High Integration, Ongoing Need)

- Description: These are roles that are central to the agency’s identity, daily operations, and long-term strategy. Examples include Account Directors, Creative Directors, Heads of Departments, and key operational staff (e.g., finance, HR).

- Optimal Model: Full-Time Employee (FTE).

- Rationale: These positions require deep institutional knowledge, consistent availability for leadership and team management, and a strong alignment with the company’s culture and values. The stability and commitment of an FTE are paramount for these foundational roles.

- Quadrant 2: Specialized Expertise (Low Integration, Episodic Need)

- Description: This quadrant covers high-skill tasks that are critical for specific projects but are not required on a continuous, 40-hour-per-week basis. Examples include a technical SEO audit for a website launch, advanced data analytics for a research project, motion graphics for a single video campaign, or specialized legal consultation.

- Optimal Model: Freelancer (Project-Based).

- Rationale: This model provides access to world-class, niche talent without the prohibitive long-term cost of employing a high-salaried specialist who would be underutilized for much of the year. It is the most financially efficient way to inject high-value expertise precisely when and where it is needed.

- Quadrant 3: Scalable Production (Low Integration, Variable Need)

- Description: This includes production-oriented tasks where the volume of work fluctuates directly with client demand. Examples are content writing, routine graphic design, social media content creation, and pay-per-click (PPC) campaign management.

- Optimal Model: Freelancer (Retainer or Project-Based).

- Rationale: Using a flexible pool of freelance talent for these functions allows the agency to scale its delivery capacity up or down in direct proportion to its revenue pipeline. This perfectly aligns costs with revenue, protects margins, and avoids the significant financial drain of maintaining a “bench” of underutilized full-time production staff during slow periods.

- Quadrant 4: Strategic Growth Initiatives (High Integration, Project-Based Need)

- Description: This quadrant addresses the staffing needs for new, unproven initiatives, such as launching a new service line or expanding into a new market. The long-term, full-time need for a role is uncertain at the outset.

- Optimal Model: Hybrid (Contract-to-Hire).

- Rationale: This approach minimizes the initial financial risk. An agency can engage a senior professional on a long-term contract basis to pilot the initiative. This provides the necessary expertise and focus without the immediate commitment of a permanent hire. If the initiative proves successful and a continuous need is established, the contractor can then be converted to a full-time employee.

This quadrant-based approach reveals that the most financially sophisticated strategy is not a choice between FTEs and freelancers, but the intentional blending of both to create a tiered, “Core-and-Flex” labor structure. This model is built around a lean, highly-utilized core of full-time employees who manage strategy, client relationships, and core operations (Quadrant 1). This stable core is then augmented by a flexible, scalable periphery of freelance specialists and production talent that can be engaged as needed to meet fluctuating client demands (Quadrants 2 & 3). This hybrid model maximizes the distinct advantages of both employment types, creating an organization that is simultaneously stable at its core, agile at its edges, and financially efficient throughout. It is a structure designed to align costs with the natural, project-based rhythm of agency work.

To operationalize this strategy and ensure consistent decision-making across the organization, the following matrix can be used by all hiring managers.

Table 3: Strategic Hiring Decision Matrix

| Role Characteristic | Key Decision Questions | Optimal Hiring Model |

|---|---|---|

| Core Business Function | Is this role essential for daily operations and long-term strategy? Does it involve managing other employees? | FTE |

| Requires Deep Institutional Knowledge | Is deep understanding of company history, processes, and culture critical for success in this role? | FTE |

| Specialized, Episodic Skill | Is this a high-skill need for a specific, time-bound project? What is the cost of this role being underutilized? | Freelancer (Project) |

| Variable / Fluctuating Demand | Does the volume of this work change significantly from month to month based on client needs? | Freelancer (Retainer/Project) |

| New Service / Pilot Program | Is this a new initiative where the long-term, full-time need is not yet proven? What is the financial risk of a permanent hire if the initiative fails? | Contract-to-Hire |

| Need for High Control/Supervision | Does the task require constant oversight and adherence to specific internal processes? | FTE |

| Need for Rapid Scaling | Do we need to increase our capacity in this area quickly without a long recruitment cycle? | Freelancer (Retainer/Project) |

Conclusion: Building a Financially Resilient, Talent-First Agency

The analysis presented in this report leads to a clear and powerful set of conclusions. The traditional debate of freelancers versus full-time employees, when viewed through a rigorous financial lens, is revealed to be a false dichotomy. The true path to sustainable profitability and strategic agility lies not in choosing one model over the other, but in mastering the art of the blend.

The key takeaways from this investigation are threefold:

- The true cost of an employee is significantly higher than their base salary. A detailed, fully loaded cost analysis, accounting for taxes, benefits, and overhead, is non-negotiable for accurate financial planning. For a professional role in a state like California, this cost can approach 1.5 times the gross salary.

- Profitability hinges on managing the utilization gap. A freelancer’s cost is directly tied to billable output, effectively making them 100% utilized on a given project. An FTE’s cost includes a substantial portion of non-billable time, which must be covered by the margins on their productive hours. This dynamic means a higher-priced freelancer can often be the more profitable choice for discrete, project-based work.

- A flexible, variable cost structure is a profound strategic advantage. By transforming labor from a fixed to a variable expense, an agency can enhance its cash flow, reduce financial risk, and build a more scalable and resilient business model capable of thriving in a volatile market.

The final strategic recommendation is, therefore, the formal adoption of a “Core-and-Flex” workforce model. This model, guided by the principles and tools outlined in the Strategic Hiring Decision Matrix, will enable AURA to build a workforce that is both a competitive advantage in the marketplace and a cornerstone of its long-term financial health. By maintaining a lean, stable core of full-time strategic leaders and augmenting them with a flexible, on-demand network of specialized freelance talent, an agency can optimize its cost structure, protect its profitability, and position itself for sustainable, scalable growth. This is the future of agency finance: a talent-first approach built on a foundation of strategic financial resilience.